Premise

The premise of this research is that NAND flash storage will replace the majority of traditional magnetic drives as the primary storage media in enterprise data centers and hyperscale cloud services over the next 10 years. Currently enterprise flash storage is less that 15% of the total NAND flash sold. The cost of NAND flash is driven by a voracious consumer market, and enterprise storage vendors adapt consumer flash to meet the higher performance and availability requirements of the enterprise.

Magnetic storage will still be a significant part of scale-out storage, supporting low access applications such as archive. The model for this is likely to be geographically distributed nodes with the metadata held on flash.

Wikibon analysis shows there is sufficient NAND flash manufacturing capacity to meet enterprise storage demand. Other storage technologies such as PCM (recently introduced by Intel/Micron as 3D XP) are unlikely to gain a foothold unless they can drive consumer demand and achieve consumer volumes. If 3D XP and other technologies do achieve critical volume, it will provide a tier of faster by more expensive non-volatile storage between DRAM and NAND flash.

Introduction

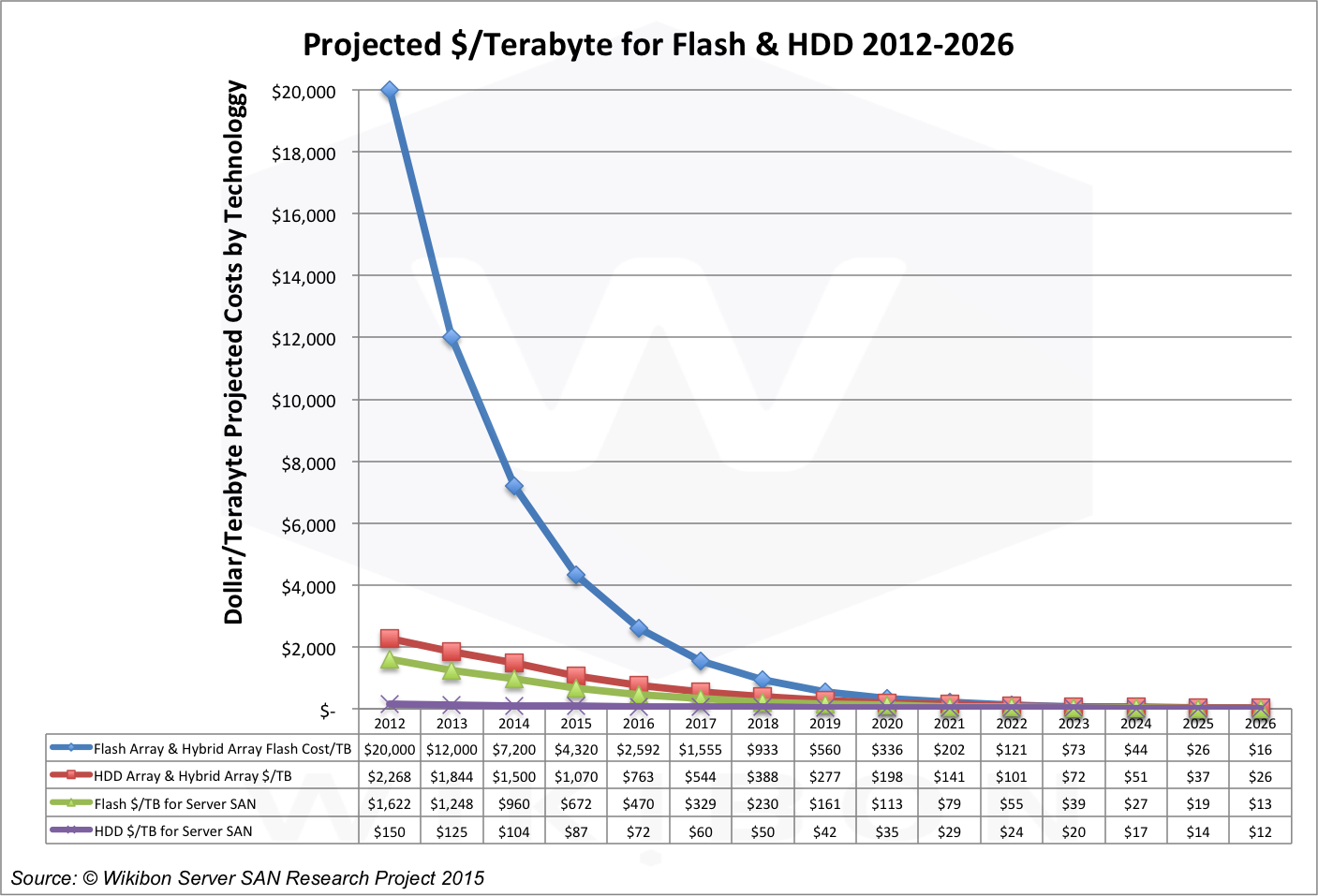

Figure 1 shows the projected cost/terabyte for traditional storage arrays (All Flash Arrays and hybrid storage arrays), and Server SAN storage. The cost/TB for flash storage and magnetic hard disk drives (HDD) are also projected. The projections show that the price umbrella of 10 times or greater over the storage media costs that protects the incumbent vendors is under severe pressure. The multiplier will come down as Enterprise Server SAN gains traction, and as more storage migrates to Hyperscale Server SAN in the cloud. This pressure will have a significant impact on the margins for traditional storage vendors, especially the newer all-flash array and hybrid storage vendors, and reward fewer vendors achieving volume and efficiency.

Source: © Wikibon 2015, Wikibon Cloud & Server SAN Project

Additional pressure on traditional storage vendors is likely to come from new storage vendors who can own the complete stack. Samsung, SanDisk and Toshiba are making significant investment in complete storage offerings. SanDisk recently announced capacity flash storage at $900/terabyte, using OpenSource software. SanDisk has joined Samsung, Intel and Micron in bringing 3D NAND flash into production. The prospect is 10 terabyte thumb drives! Intel and Micron have announced a much more expensive but higher performing non-volatile 3D XP technology which may eventually make it into production for very high performance machines.

Overall Server SAN Adoption Projection

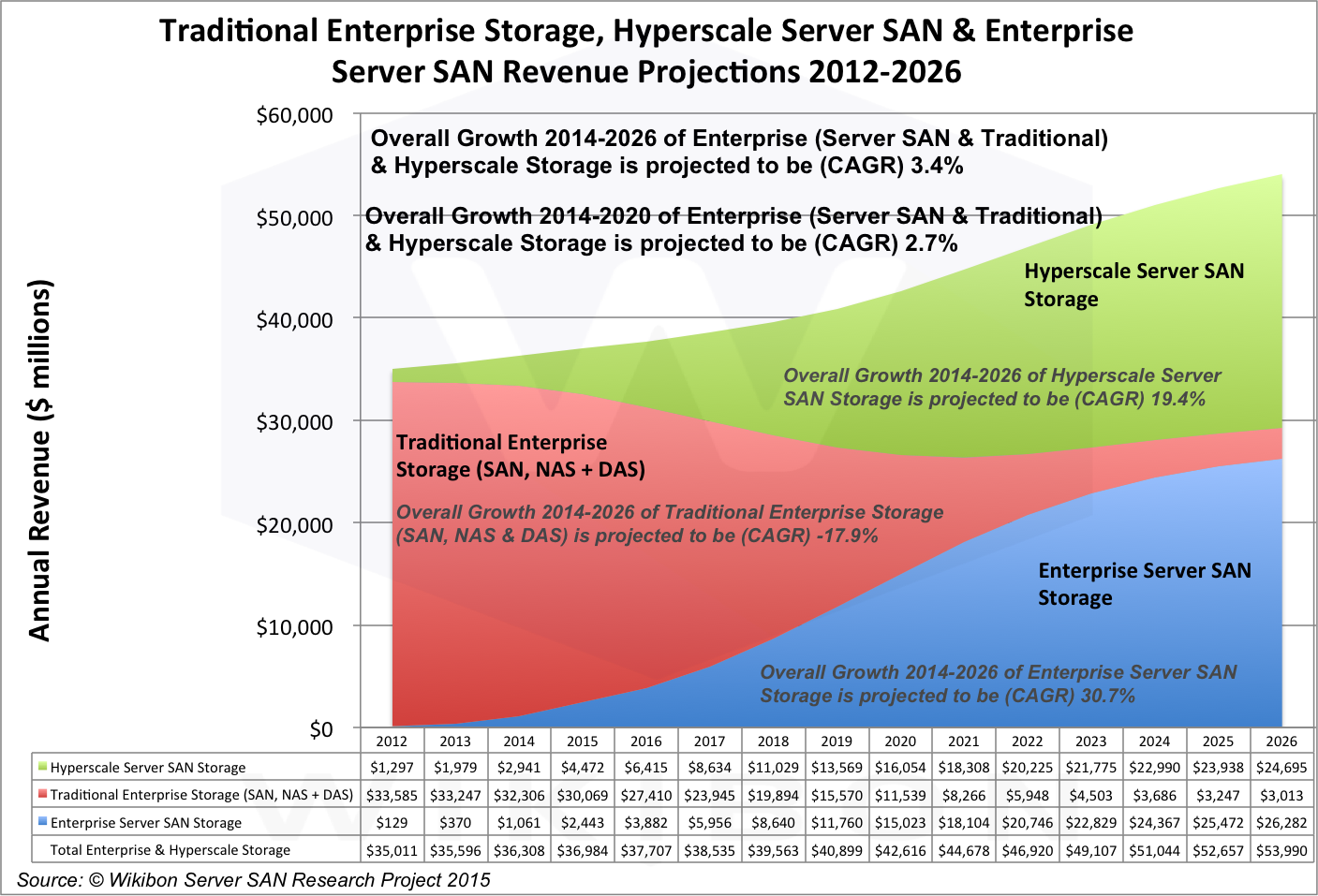

Figure 2 is the overall Wikibon projection of traditional enterprise storage, Hyperscale Server SAN (large-scale usually supporting cloud services) and Enterprise Server SAN. The projections show very clearly the vice grip the two types of Server SAN are applying to traditional storage and traditional storage vendors.

Source: © Wikibon 2015, Wikibon Cloud & Server SAN Project

Overall Flash Adoption Projection

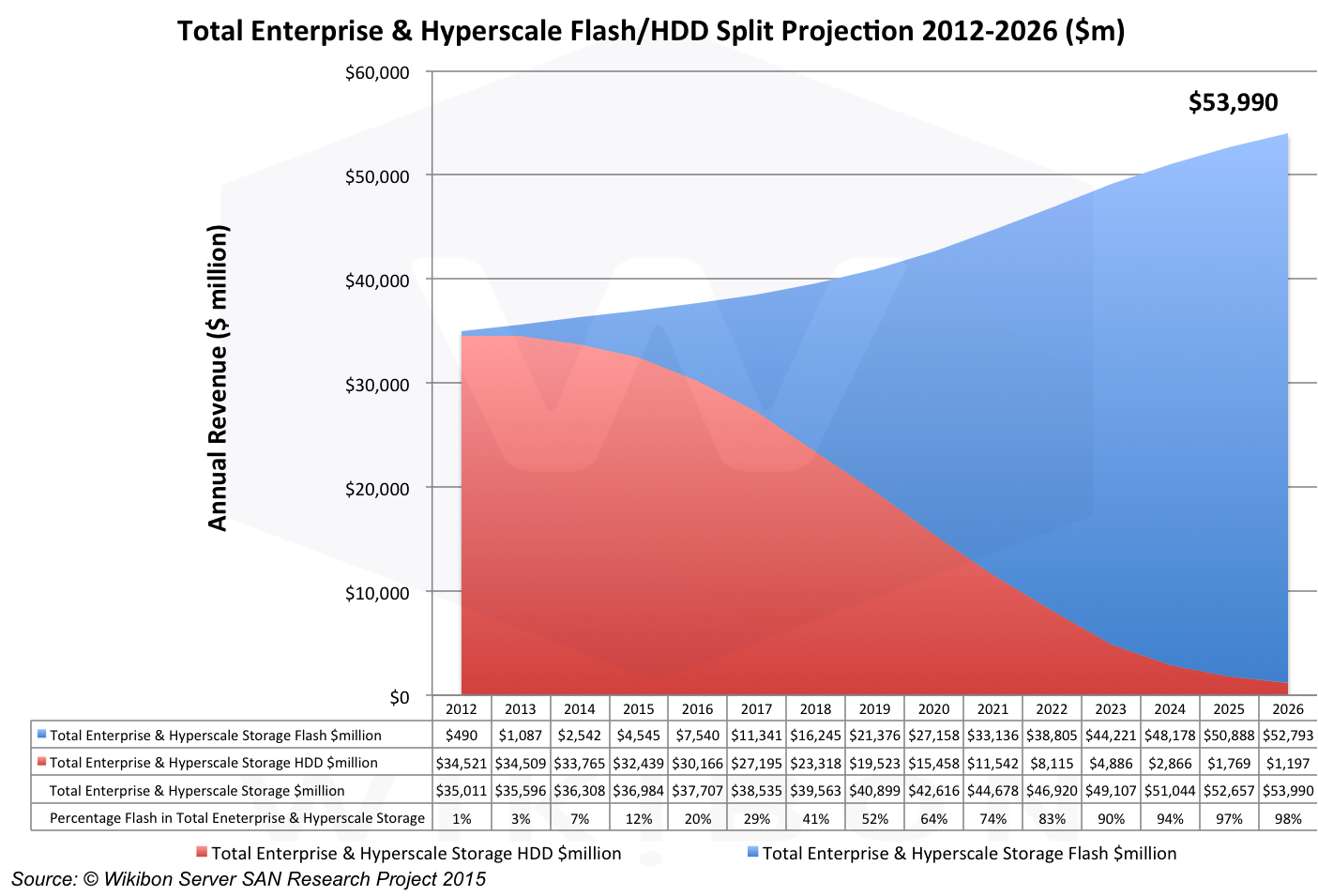

Figure 3 shows the overall split of between flash storage revenues and traditional magnetic storage revenues. Like all great technologies, magnetic storage in general, and the magnetic disk drive in particular, has a long ride into the sunset. Magnetics are a cheaper way of holding WORN data (write once read never). Magnetic tape libraries provides excellent bandwidth together with flash holding the metadata (Flaps). Magnetic disks with spin-down and metadata on flash provide low-cost for many years, and random access to data. Over time, all useful data will migrate to flash, and magnetics usage will be focused on mainly archive data.

Figure 3 is the sum of the data in Figures 4, 5 & 6 below, which represent the flash adoption within Enterprise Server SAN, Hyperscale Server SAN and traditional enterprise storage.

Source: © Wikibon Server SAN & Cloud Research Projects 2015

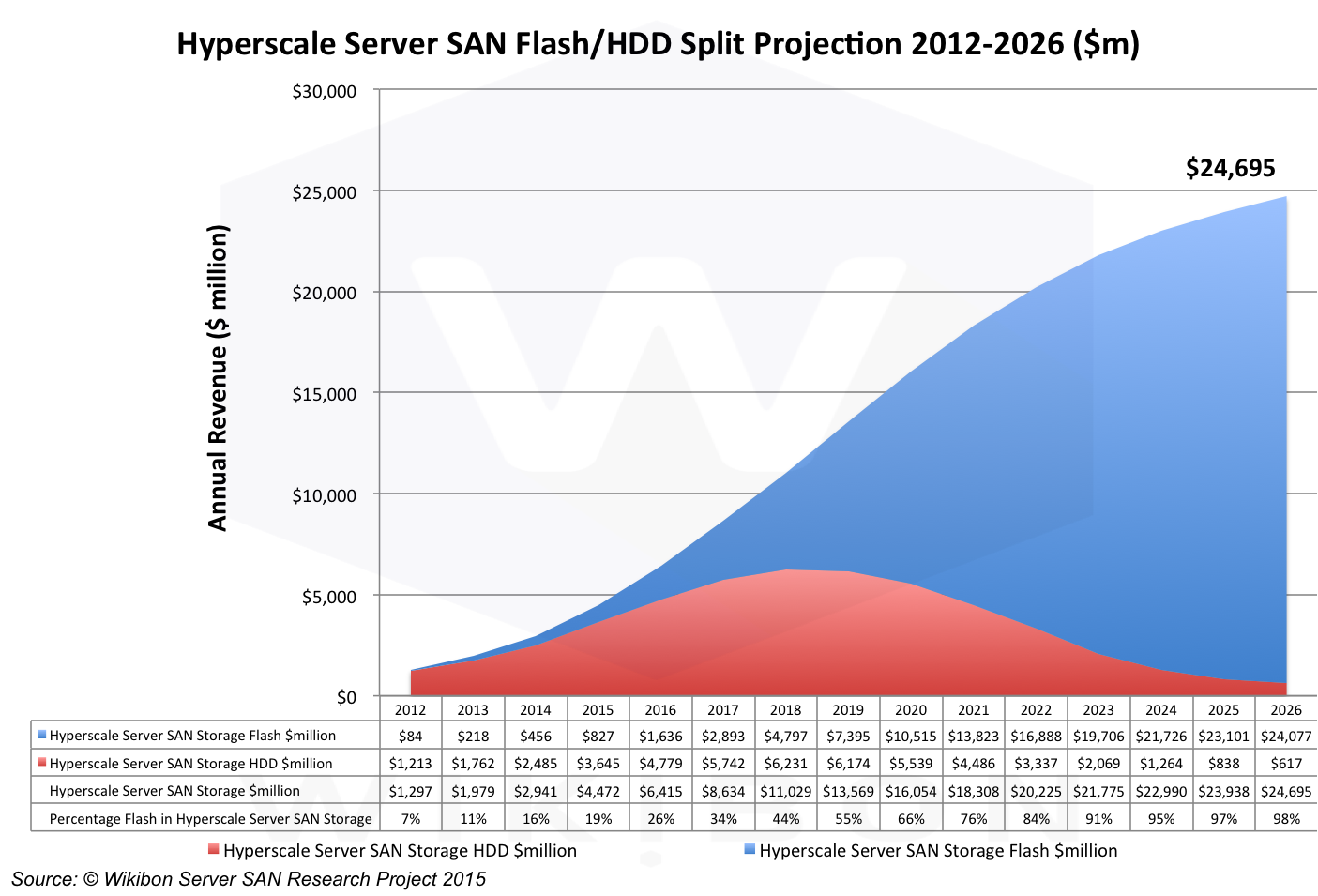

Server SAN Flash Adoption Projections

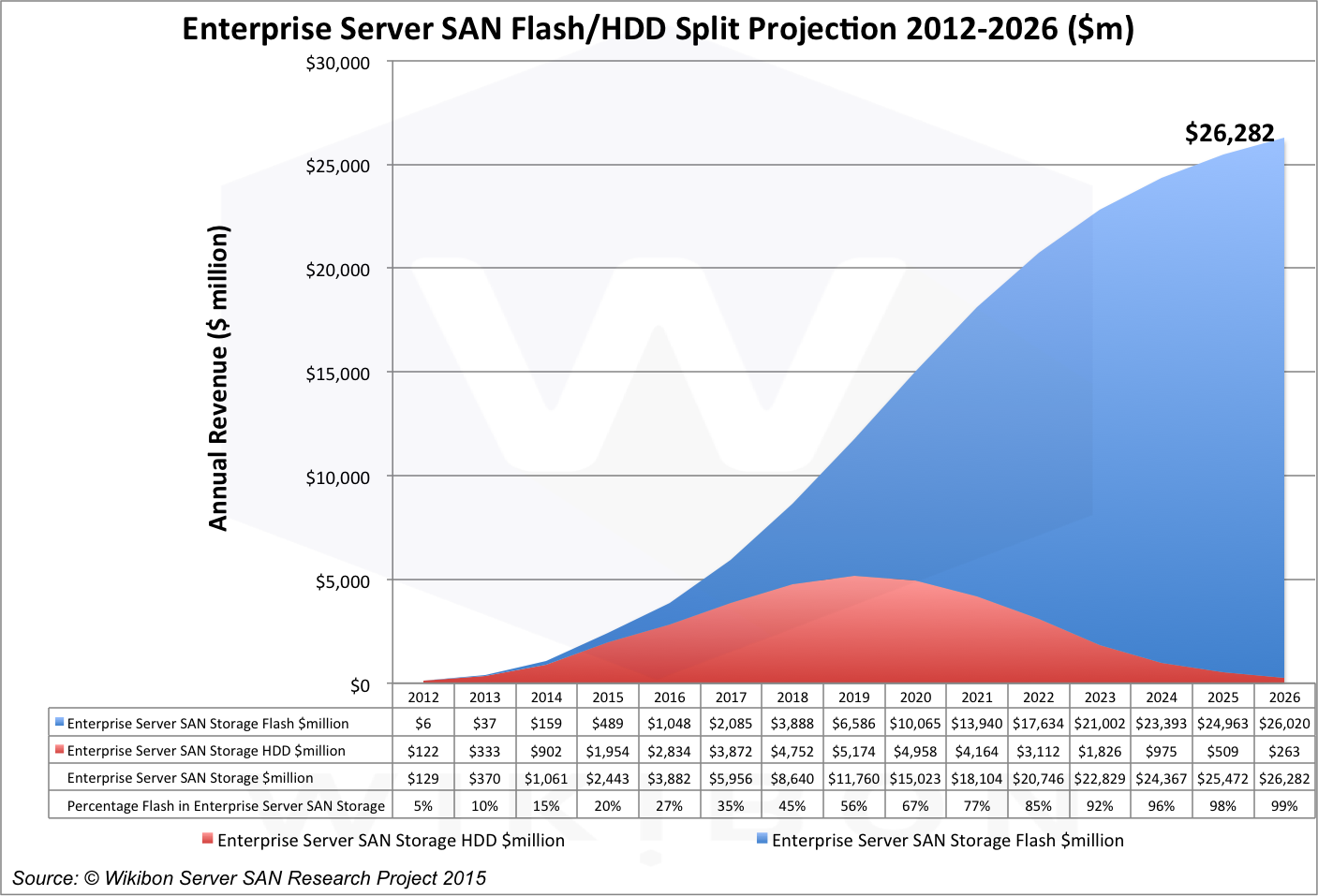

Figure 4 and Figure 5 show the adoption of flash within Enterprise Server SAN and Hyperscale Server SAN.

Source: © Wikibon Server SAN & Cloud Research Projects 2015

Source: © Wikibon Server SAN & Cloud Research Projects 2015

Within Server SAN the same adoption shape is seen, with traditional magnetic disk taking the lions share of the initial growth, and then tailing off as flash become relatively lower cost and much higher function.

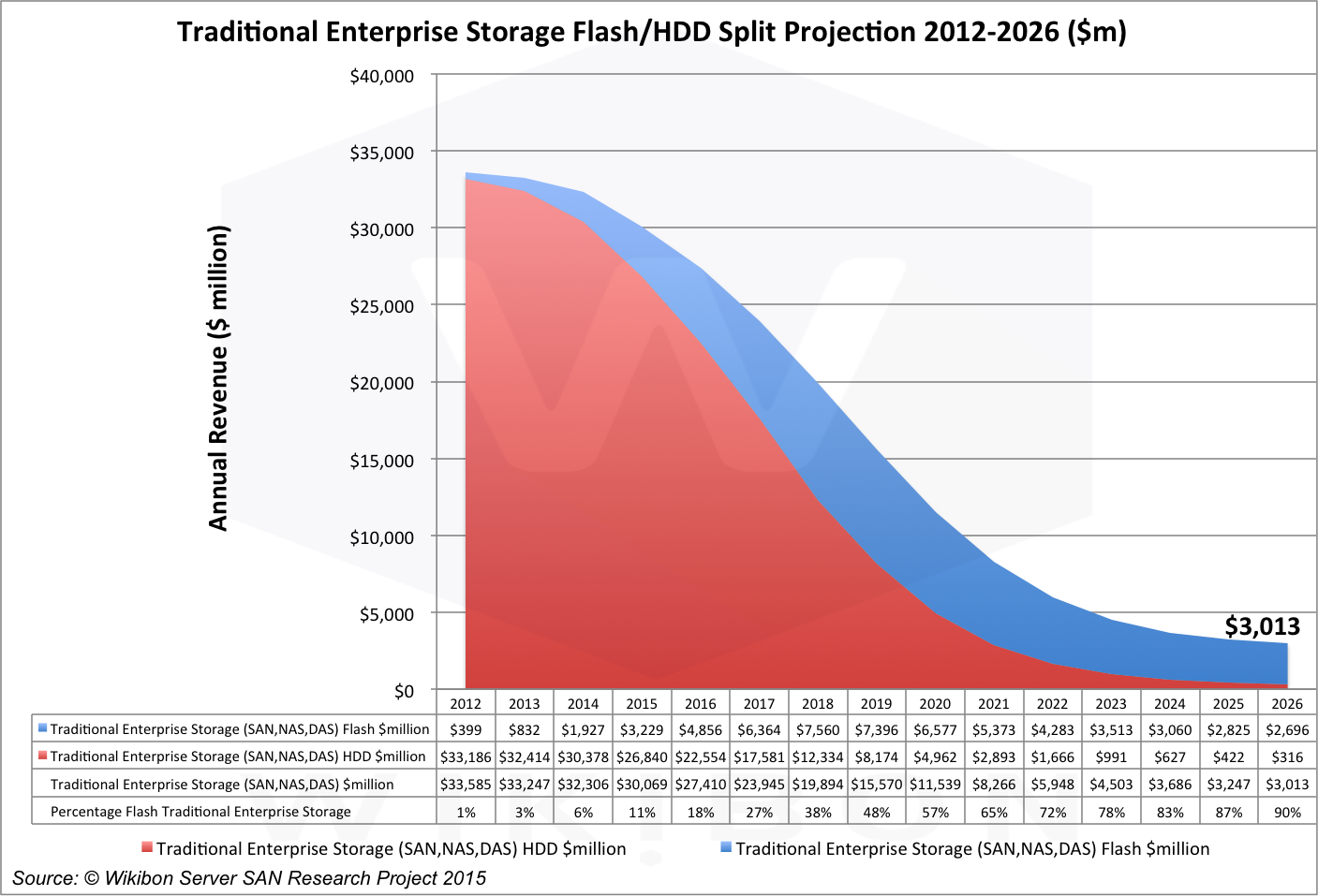

Traditional Enterprise Storage Flash Adoption Projection

Source: © Wikibon Server SAN & Cloud Research Projects 2015

The flash adoption within traditional storage come from SAN and NAS All Flash Arrays and hybrid storage arrays with a combination of flash and traditional magnetic HDDs. Figure 6 shows the adoption of flash within traditional enterprise storage. The constraint on growth of flash within traditional enterprise storage is because of the lower cost and higher performance of the Server SAN model. As can be seen in Figure 1, the cost of traditional SAN/NAS storage with flash still reflects the higher cost of bespoke software for each individual array.

A second major constraint of conversion to flash-only storage is migration of application, middleware and infrastructure software that will support and exploit flash. The third is the slow adoption of changes in operational organization and procedures required for flash-based Server SAN. NAND flash storage requires very different operational principles and procedures. For example, traditional magnetic hard disks have a very low ability to support multiple users and usage, and data has to be copied many times. Flash allows logical sharing and multiple usage of the same physical data because its superior IO characteristics, which significantly reduces the number of copies required. Traditional synchronous and asynchronous replication can be replaced by much faster and more flexible crash and application consistent snapshots, enabling much improved RPO and RTO SLAs at much reduced costs. These changes will take significant time and effort, and will be a constraint on adoption.

However, the rapidly lowering cost and higher performance of flash will result in a rapid adoption of flash to replace magnetic drives. Flash together with Systems of Intelligence will enable the integration of big data analysis into operational systems, and automate many decisions.

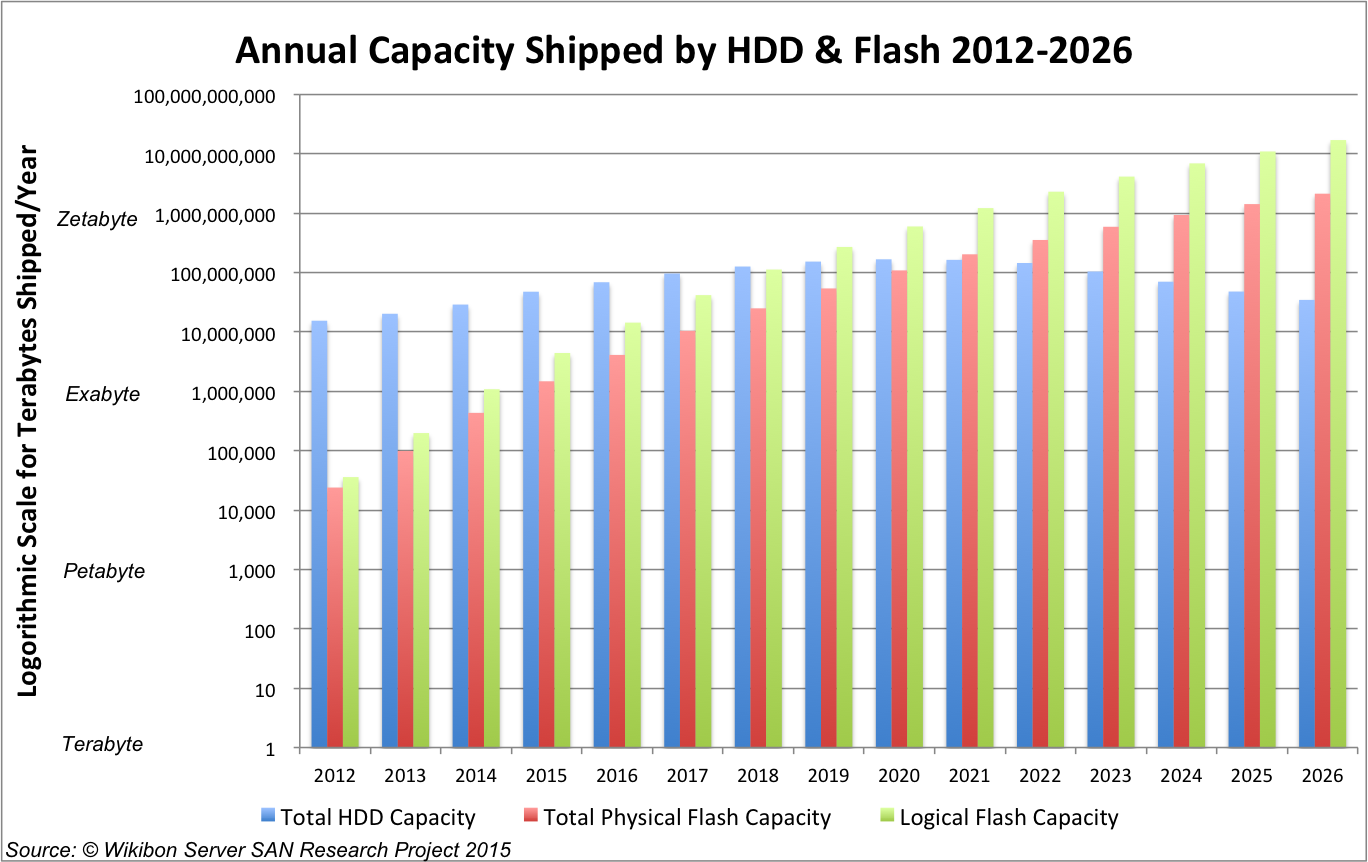

Storage Capacity Shipment Projection

Figure 7 shows the annual capacity shipment projections from 2012 to 2026. The capacity shipments from magnetic disk media (blue bar) are 1,000 times greater than flash in 2012 (red bar). The green bar shows the logical capacity shipped, i.e. the amount of storage that the users see as theirs, even though much of the physical data is shared with other users. The multiplier between physical and logical starts at 1.5 in 2012, and grows to 8 by 2026.

Flash is projected to ship the about same amount of logical flash as magnetic disk in 2018. The amount of logical flash capacity shipped in 2026 is projected to be about 1,000 times greater than traditional HDD.

Source: © Wikibon Server SAN & Cloud Research Projects 2015

Action ITEM

CIO and senior storage executives should be planning to move from HDDs to NAND flash storage over the next few years, and plan completely different organizational and operational environments. The traditional SAN and NAS enterprise storage should be migrated to Enterprise Server SAN or Hyperscale Server SAN cloud services. The ability to provide multiple logical views of the same physical data will be a key capability that will significantly simplify data movement and significantly reduce costs. Most magnetic storage for enterprises will be found in distributed cloud services for mainly archive-type applications.