An AI-powered rebound in semiconductor stocks has many investors asking if this is a harbinger of good news for the broader enterprise tech sector. Indeed the SOXX semiconductor ETF is up nearly 30% year to date as of this posting, as are bellwether fab suppliers like Applied Materials and Lam Research. Nvidia is up over 90% YTD and AMD over 50%. Even the beleaguered Intel is up 22%. But key enterprise software names have not yet rebounded and according to this week’s guest, the divergence between semis and B2B software is getting hard to ignore.

In this Breaking analysis we examine the the bifurcation between the performance of semis and broader enterprise tech. And we’ll try to answer the question: Is the uptick in semiconductors an early indicator of a broader enterprise tech recovery, or is this a false signal that warrants continued caution? To examine these issues we welcome back Ivana Delevska, the founder and chief investment officer of SPEAR Invest.

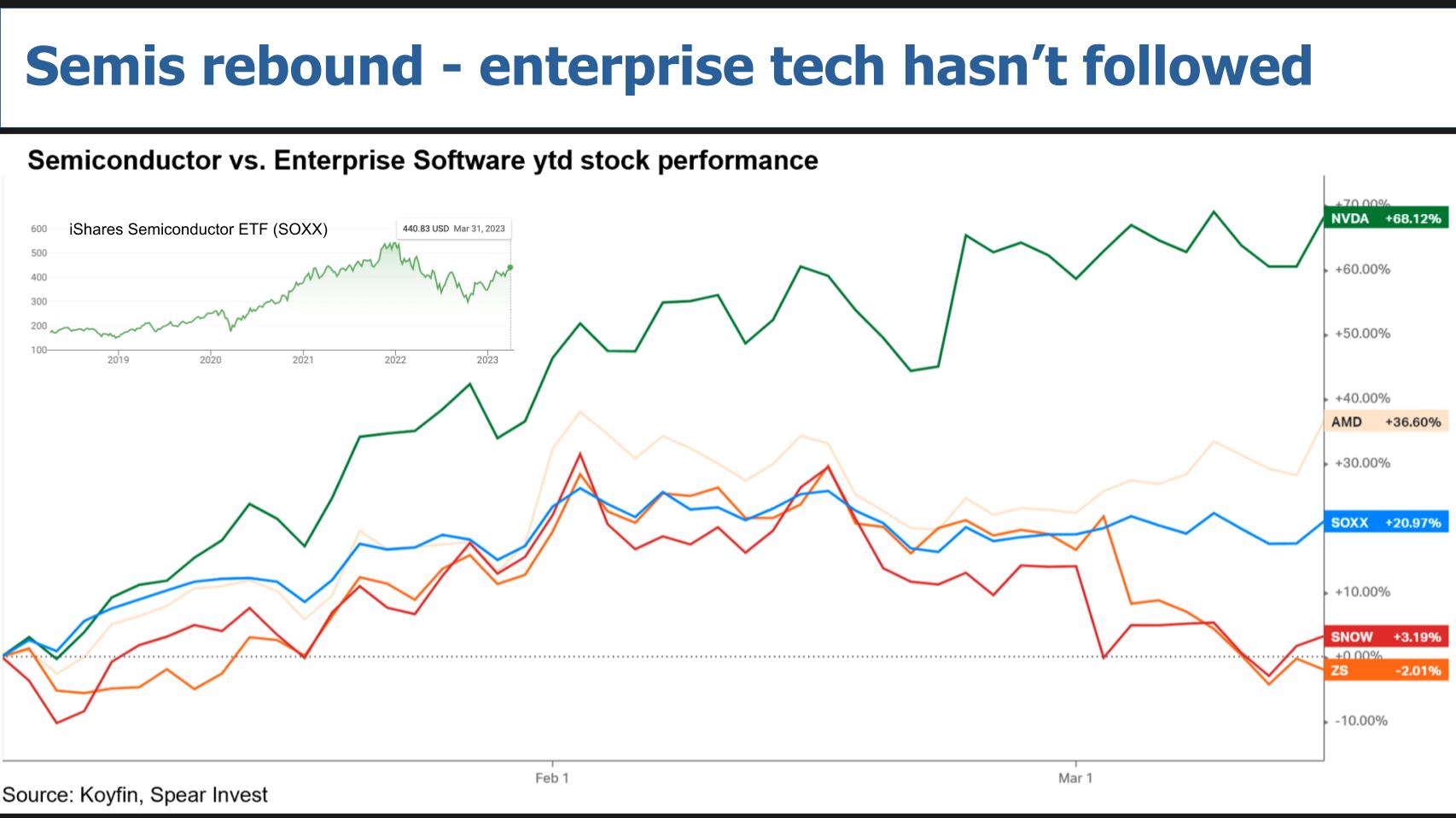

Semiconductor Stocks Outperforming Broader Enterprise Software

When SPEAR Invest last came on Breaking Analysis we talked their investment thesis of buying the dip for names like Coupa, Snowflake and Zscaler. That strategy worked for a few more months until the market shifted. We asked Ivana if she’s changed her investment strategy.

We haven’t really changed courses. What we try to do throughout a downturn is keep adding risk slowly. So we’ve just kept adding to these names, with the expectation that once the market settles, these are pretty high-quality names; they will outperform. Similarly with the semi stocks, we kept adding throughout the downturn. NVIDIA became one of our largest positions. And as the market rebounded for semis, which are usually early cycle, that’s been been helpful to our portfolio.

[Listen to Ivana Delevska explain her investment thesis].

Is a Rebound in Semis Reason to Reset Expectations for Broader Tech?

The catalyst for this Breaking Analysis was a research post SPEAR put out on LinkedIn asking if the semi rebound spells good news for broader enterprise software. In that note SPEAR showed the chart above which is pretty self explanatory – you have Nvidia, AMD and the SOXX ETF significantly outperforming two names SPEAR owns, Snowflake and Zscaler.

Note that Wikibon inserted a chart of the SOXX ETF just to show how cyclical semiconductors are and have been for years – we forget that sometimes.

Ivana Delevska shares the premise of her most recent research as follows:

You’re spot on in terms of the cyclicality of semis. Usually, semiconductors are sold through the channel. So that’s why you see these wild swings. Basically what ends up happening is the companies [end customers] themselves have very limited visibility, while the channel has a lot of inventory. So once you see a small deterioration in demand, you’re going to see an exacerbated impact to a [semi] company’s revenue number. So going into the second quarter of 2022, we saw a pretty significant downside: 40, 50% in terms of revenue declines in some segments for the semiconductors. And as we’re coming out of it, we’re seeing the opposite dynamic happen. So you are seeing the market stabilize, but the channel inventories are pretty low. As those [inventories] need to be rebuilt, you’re going to see an uptick in demand.

[Listen to Ivana Delevska explain why semi cyclicality can often predict market moves].

The Impact of Foundation Models on Semiconductor Demand

Sticking on semis for a minute, we wanted to understand how SPEAR sees AI and large language models supporting the semiconductor resurgence? You’ve got all this innovation driving semiconductor demand, EVs are a hot area that contain twice the semiconductor content relative to conventional vehicles and you have geopolitical forces driving investment such as the chips act. Semis peaked toward the end of 2021. We asked Ivana Delevska if this a cyclical rebound in her view or is it a false positive? She responded as follows:

Semis usually have a cyclical and a secular component. The secular component hasn’t really changed since two years ago or even since five years ago. As we need more compute power, we need more hardware on the backend. So it’s a pretty simple thesis. We believe that at this point in time, there is a cyclical operator, and the secular drivers are kicking in pretty strong, driven by AI. So we believe AI will be a significant driver. And a lot of people are asking, “Well, is this just the hype? And is it really showing into numbers?” And the answer is yes, it is already showing into numbers. And you can see that NVIDIA’s data center segment is outperforming other data center, that other data center spend. So we are already seeing it.

Not as strong as to justify the stock price move just yet, right? So we do need to see a few more quarters of improving data center demand. But we are already seeing the early benefits of AI in NVIDIA’s numbers.

The last semiconductor name that SPEAR added to its portfolio is AMD. SPEAR believes that as demand grows, NVIDIA is going to remain a market leader, but supply is going to get so tight. Ivana Delevska points out that we’re already seeing this from many companies, even Microsoft, having to prioritize its AI usage in compute-intensive projects. As well, Nvidia’s CTO publicly stated that they’ve prioritized AI over crypto. The point is SPEAR believes there is going to be a broader benefit to GPU manufacturers, including AMD which offers lower cost alternatives to Nvidia’s high end GPUs.

[How Ivana Delevska sees Nvidia’s CUDA architecture as a ‘moat’ in AI].

Ripple Effects of Changing Cloud Tides

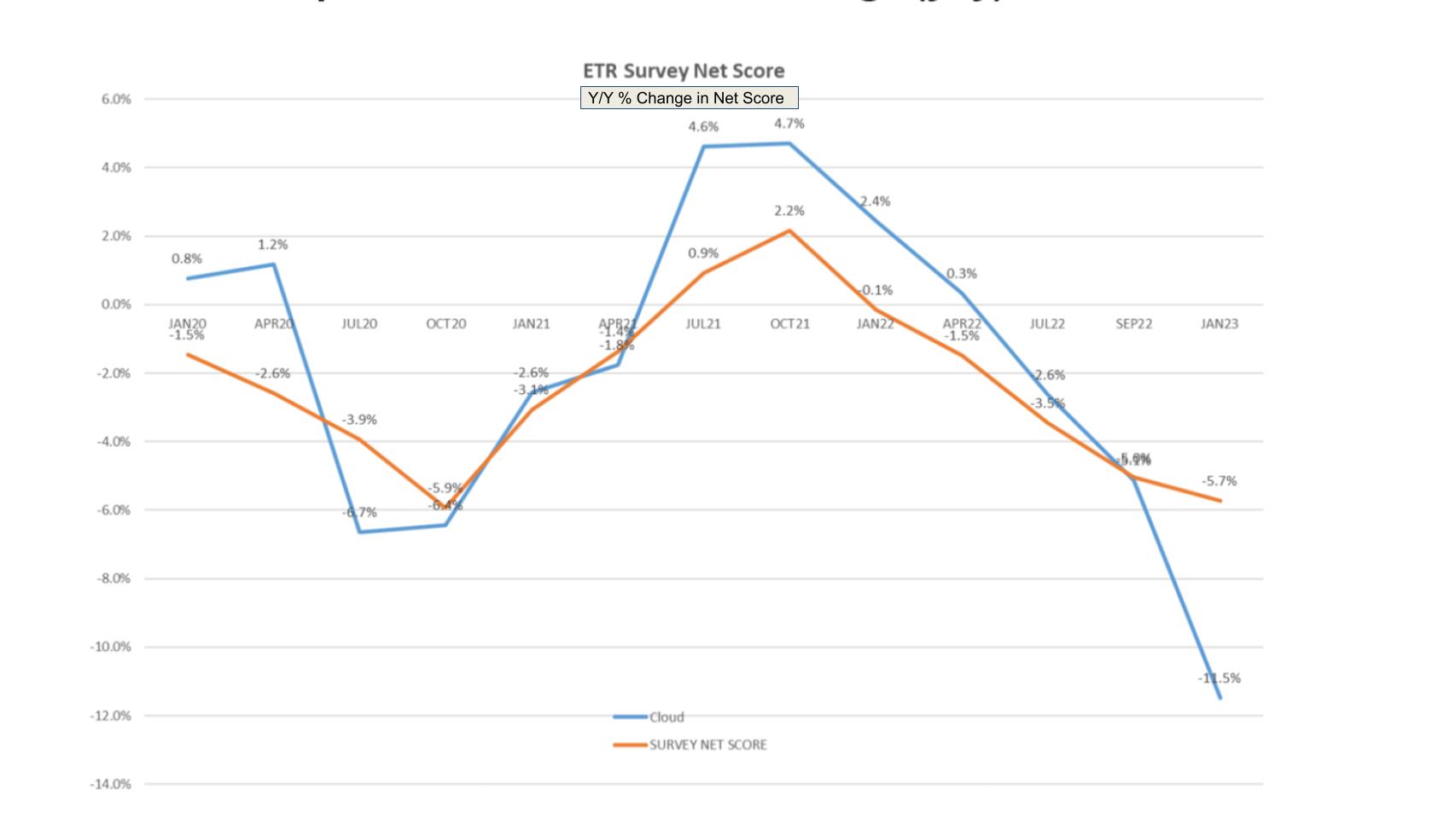

One of the factors suppressing enterprise tech is cloud optimization. Below is a chart from ETR that underscores this trend.

The chart above is from an ETR Tweet which shows the percent change in Net Score. Net Score is a measure of spending momentum. The blue line is the change in sequential cloud spend and the orange line is the change in overall survey Net Score. This data is from approximately 1,400 respondents. The message in the data is cloud has essentially dragged down the entire industry because cloud spend is a much higher proportion of tech spend today than it was during the last big downturn in 2008/2009. Because cloud is so much easier to not only dial up…but also dial down, cloud optimization has created a downdraft across enterprise tech.

Delevska sees AI as a catalyst, along with cybersecurity spend, as supporting tailwinds to her thesis. She continued as follows:

AI requires a lot of data. And what we believe is going to end up happening is that the compute power is going to become really expensive. So it’s going to be all about optimizing how you’re doing the processes, where you’re running the processes. So we really like companies like Snowflake, for example, that will help you choose where you want to run the compute, where you want to do the storage. So we believe it’s the same thing with cybersecurity. As you introduce AI, especially in real-world applications, like if you’re remote monitoring a refinery or you’re doing predictive maintenance on some of these large real-world assets, cybersecurity is going to become crucial. So we believe these are really strong long-term drivers for both of these segments. And you don’t really hear the CEOs talk about these trends on their conference call, just because it’s a little too early to see it reflected in the numbers. But there is no question that this is going to be a long-term driver.

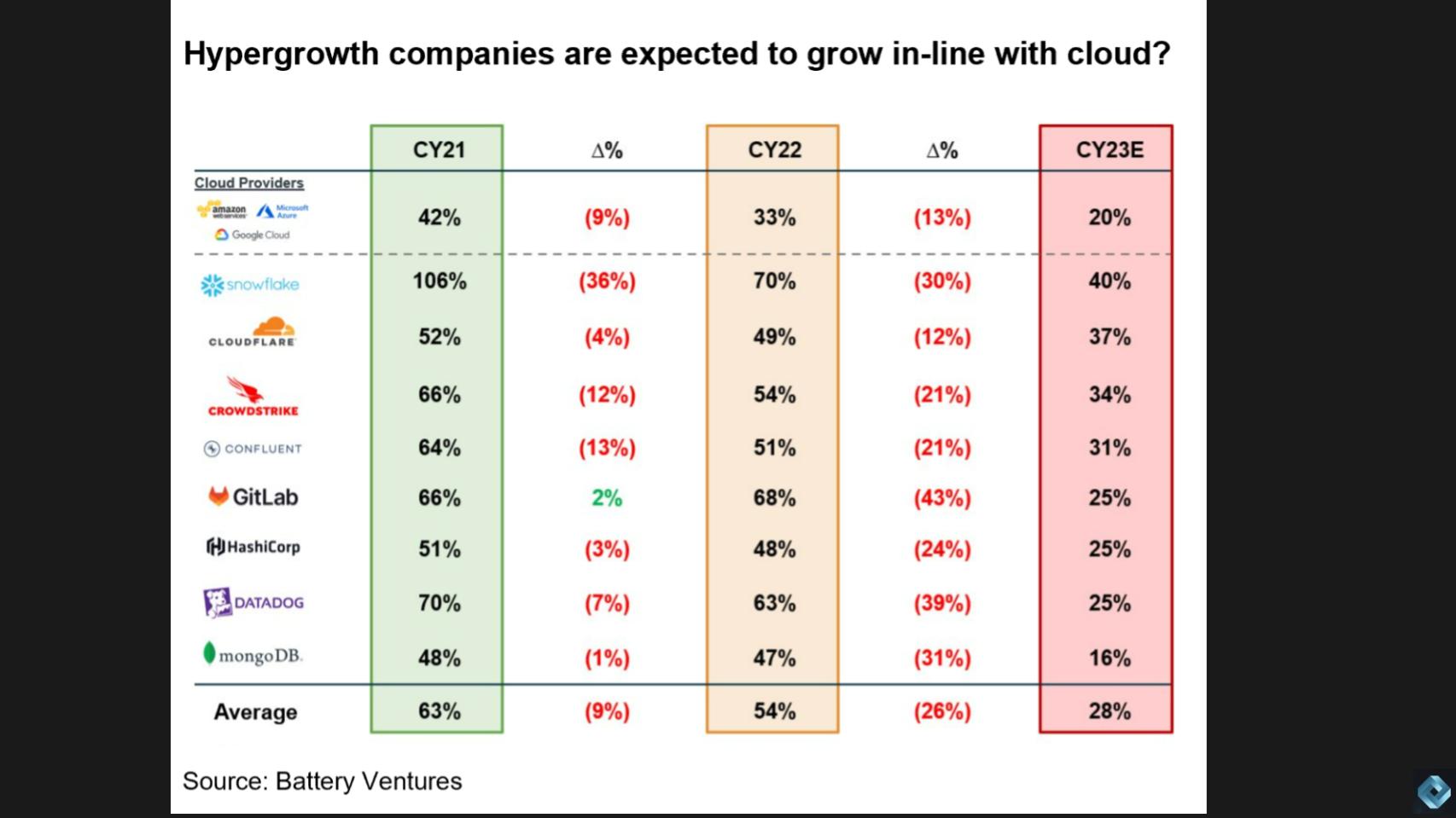

How Hypergrowth Tech has Slowed & is Tracking toward Cloud Spend

The chart below shows the calendar 2023 forecast for the hyperscalers as a group – growing 20%, then Snowflake at 40%…all the high fliers – Cloudflare, CrowdStrike etc… all the way down the list averaging out at 28%. This is well off the expectation of 2020 and 2021.

But there’s still some momentum in pockets. We saw CrowdStrike’s last earnings report was positive. Palo Alto Networks is not shown above here but surprised to the upside. Cisco beat and raised so it’s mixed between positives and negatives.

We asked Ivana Delevska her thoughts on how much upside is in this data because you have easier compares and conservative guidance. And we wanted to know how much conservatism is in these numbers. She made the bull and bear case as follows:

We believe there is absolutely some level of conservatism built into these numbers. Enterprise spend, a lot of it is driven by sentiment. So if people are feeling good at the companies, they’re going to decide to budget more for next year. If they’re scared about the economy, they’re not going to budget as much. So it’s unlike semis where it’s driven by real demand. Like if people are buying GPUs, you’re going to see it in the numbers. Enterprise spend is a lot more sentiment-driven. So at the moment you saw some weakness in the economy, CEOs and CTOs started cutting their budget. So we believe there is some level of conservatism in these numbers.

The bigger shock looking at that table is that a lot of these hypergrowth companies with really interesting products are starting to show growth rates close to the cloud vendors, which doesn’t quite make sense. So we have a lot of mature companies as well that we’re following. And growing at 20%-plus is really not that difficult if you have an innovative product. So I think that not only that these numbers are conservative, but the real problem here is that when people look at 20, 25% growth, is that going to be then stepping down to 15 and then down to 10? Because that’s a big problem. So that’s kind of what you’re having priced into the stocks today. Or is that going to be something that we are seeing one year of weakness, and then it resumes in the 30s in terms of percentages? So that’s the big delta I think between the bears and the bulls today. If you think this is the new level of growth and these hypergrowth names grow at 20%, no, you can’t even justify the valuations today, right? But if you believe this is a cyclical downturn, which is the camp that we are in, and they can get back to a more normalized level of growth, then they look very attractive here.

[Listen to Ivana Delevska make the bull and bear case for enterprise B2B tech].

Can Hyperscalers Return to Hyper-Growth?

Currently, Wikibon hyperscaler forecasts show 2023 at around 15% revenue growth for AWS and 21% collectively for the big four. We asked Ivana Delevska for her take on whether hyperscaler growth could return to higher levels. Her response:

There is no question that this is a cyclical downturn. So I think a lot of investors, what they miss about hyperscalers is that their business model is in a way taking risk away from the consumers and onto their balance sheet, right? So you are supposed to be seeing a cyclical slowdown because people do reduce consumption. So it’s almost like the business model itself, the value proposition that they have for their customers is that they can scale up and scale down. So I do believe that we’re going to see a cyclical re-acceleration from these levels. I don’t think we’re going to see 40, 50% growth, which I think some of the other names that are coming from smaller bases and smaller scale, I think they could return to those types of levels of growth.

[Ivana Delevska explains her thoughts on hypersalers and they’re prospects for hyper-growth].

Will Security be a Catalyst Similar to AI?

The security sector is up year to date but some names, like Zscaler are lagging. Then you have CrowdStrike and Palo Alto surprising to the upside. Security remains the #1 priority of technology departments and specifically zero trust is becoming a watch phrase that increasingly has meaning. We asked Ivana Delevska – Will security lead the rebound in enterprise software?

I don’t know about leading the rebound, but I do absolutely believe that we’re going to return to more rapid growth. Basically, the big problem right now that we hear from our companies is that they’re having trouble getting new customers to sign on. So this is why you see platforms like Palo Alto and CrowdStrike outperform, because they already have a pretty large installed base of customers that they can upsell products to, rather than having to go out there and find new logos where a lot of the weakness is.

[Ivana Delevska explains the prospects for cybersecurity leading a rebound].

The Semi Rebound Doesn’t Show up in IT Spending Trends

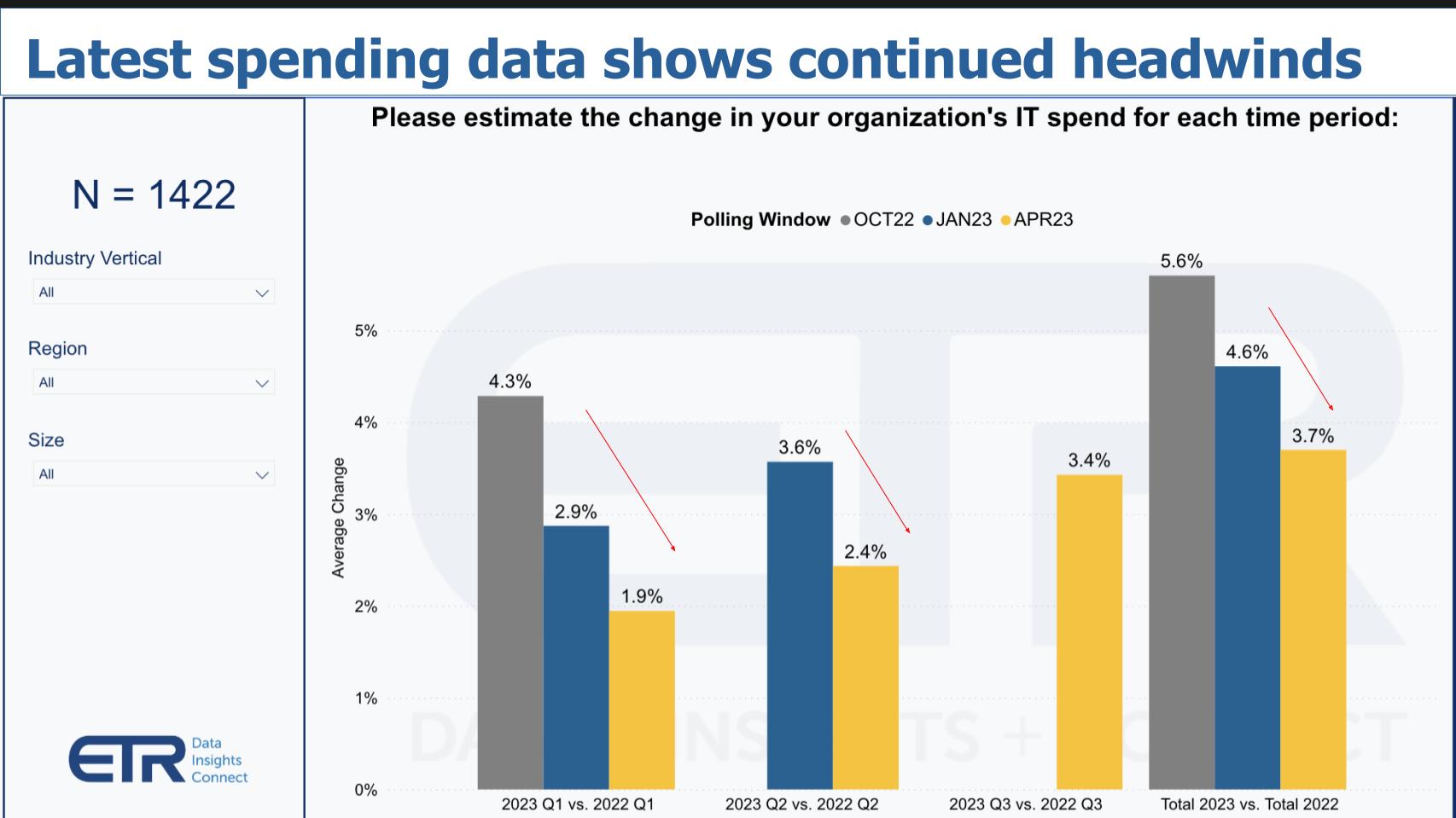

The last data slide we want to share is preliminary data from ETR’s latest survey. We got permission from ETR to show the data below from the very latest quarterly TSIS survey which is still in the field but almost complete.

Coming into January 2023, the expectation from IT decision makers (ITDMs) as you can see on the far right set of bars, was for spending to increase 4.6% (the blue bar). That’s now down to 3.7% (yellow bar). What’s more, the buyers have changed quite a bit in terms of techniques they’re using to cut. Up until this survey the focus has been on consolidating redundant vendors and optimizing cloud costs. But digging into the ETR database (not shown here) it appears that organizations are turning to other techniques. Specifically, delaying or canceling new projects is now #1, cutting staff, reducing hardware spend and spending less on consultants now comprise the top four techniques to save money, eclipsing consolidating redundant vendors and optimizing cloud spend.

Delaying or canceling new projects, cutting staff, reducing hardware spend and spending less on consultants now comprise the top techniques to save money, eclipsing consolidating redundant vendors and optimizing cloud spend.

Our view is this data suggests we still have a ways to go because if buyers are canceling projects and cutting staff, restarting them will take a bit of time.

We asked Ivana Delevska to square the circle between her premise that semis are a leading indicator of a rebound and how ITDMs are behaving. Her response follows:

I do think a lot of this data is based on companies [end customers] which are still pretty cautious. So a lot of it is sentiment-driven. It’s going to be very different industry by industry. I just met with over 50 industrial companies with pretty broad end markets and sub-sectors ranging from aerospace, housing, raw industrials, mining, and all those end markets are doing really well. So all of those companies are going to now reaccelerate spending, even though they were cautious maybe three months ago. So I think it’s going to really depend industry by industry. Banks obviously are now in focus and are not doing well. So a lot of people are asking, “Well, is that really the next shoe to drop here?” For companies likes Snowflake, banking and financial services industry is a pretty big end market.

But I do believe it all goes back to the economy. And if you start seeing the consumer doing a little better and the industrial economy reaccelerating, all of these other sectors will just have to follow. So we do quite a bit of channel checks to get a framework of where things stand. And things are actually a lot more optimistic than what you hear on TV.

[Ivana Delevska explains how she sees end market dynamics and how a recovery might take shape].

Three Trends in Focus as Upside Catalysts

Spear is focusing on market dynamics in three areas and looking for companies that can capitalize as shown above. We unpacked each with Ivana Delevska and asked for some examples of tech companies that could benefit.

Platforms Beat Point Products

Basically, these are trends that we’re seeing already today. Companies like CrowdStrike, who would consider them as a platform, where basically the company started as an endpoint leader; they gained a pretty significant market share. So they got to a point where if you analyze it, you’re like, “Where is the upside going to come from?” Well, now they’ve expanded into several different areas that could be providing a pretty significant total addressable market expansion. And they’re in addition expanding to small and medium businesses. They just announced a partnership with Dell, where you can have CrowdStrike available when you purchase your computer, which is a pretty big deal. So it’s really all about finding products where they can use the same infrastructure and sell more products and more services.

[Watch the clip explaining why platforms beat products and which companies benefit].

Cost Cutting as an Upside Catalyst

There is a bifurcation. If somebody’s cutting 10% of costs, of workforce, it usually means that their products are still working, demand is still there: they’re just optimizing. So that’s usually like the area that you’d want to focus on, because you can get some pretty low hanging fruit. And even as the market continues to recover, they will continue to benefit from the great products that they have. So HubSpot is an example here. They are obviously seeing some slowness compared to history, but they’re still growing at pretty attractive rates. So now once they optimize their cost structure, over time that’s going to be pretty meaningful for margins.

Where we are more cautious are companies that are cutting more than 20% of their workforce. This is usually a sign of something really bad going on, right? Like you’re either, thought you had a business, but that business is no longer viable, right? So here you can still find some good opportunities if somebody is able to turn around what they’re doing. And Meta is I think one that could fall into this category. We are not involved. But you could see them maybe able to successfully transition to a lower cost structure. But it is a red flag for many others. Like Upstart or Opendoor also had a pretty big workforce cut. Carvana I think was also as well over 10%. In these cases there may be a business model challenge, right? And you don’t want to be stuck with these ideas where you get a pop in the first year, right, when they actually do show margin improvement. But if the business model is not there, how are you going to generate the returns in the long term? So we prefer to stick to the ones that we consider to be quality, and the cost cut just enables them to have a efficient operating model going forward.

[Which companies potentially signal danger when it comes to severe cost cutting].

Must Haves vs. Nice-to-Haves

Cybersecurity is an area that is a must-have. So even if you push out a project or you split it into different pieces, eventually you’re going to have to do it. Similar with cloud spending. Optimization, yes, pretty meaningful, a significant negative driver to results, but there is only so much you can do. So those areas also are very difficult to cut beyond just optimizing. But there are a lot of small tools that are supposed to be improving productivity that are not in that must-haves camp, right? So they do need to prove out their business model. And maybe they’re not going to get a chance in this type of a market. So a lot of this we see in DevOps, basically where you are providing useful tools, but the question is: Does the CEO really understand what the ROI on that is?

And is there even an ROI? Some of them may not really be offering the productivity improvement that you think you’re getting. So we do prefer the must-haves. I think that’s a really good way to manage risk, where these companies are still going to provide a lot of upside if the market turns. But in the meantime, they do generate free cash flow, and they do fall into this more defensive camp.

[How to play the thesis around must have vs. nice to have].

Managing Risks to the Rebound Scenario

We want to close by asking what are the risks to the SPEAR scenario? We have the banking crisis and a potential liquidity crunch. Could the semis retrace 10-20% given the run up? Is chasing broader tech ‘fools gold’ at this point or are semis a leading indicator and six months ahead of the curve? The following paraphrases Ivana Delevska response:

The biggest risk currently is the potential liquidity crunch faced by small businesses, as large enterprises such as Airbus and Boeing don’t face the same cash flow problems. Interestingly, the real liquidity crunch took place a year ago, with the downside already priced into the market. When interest rates rose, small businesses became more cautious. This has led SPEAR to a more optimistic outlook, with the belief that the liquidity problem will not be as severe as initially anticipated.

In the semiconductor industry, despite strong fundamentals, there is the possibility of a 10-20% pullback due to market volatility. The ongoing recovery in China is expected to drive the next phase of growth for semiconductors.

However, the most significant risk overall is the likelihood of a more muted recovery compared to past instances, which can be attributed to high rates and limited demand growth. As such the recovery could be choppy and elongated, perhaps over several years.

[Watch this clip of Ivana Delevska’s commentary on risks to her investment scenario].

On balance we’re encouraged that SPEAR’s fundamental investing approach hasn’t changed. Rather Ivana Delevska has added risk more selectively betting that the upside will eventually pay dividends. We’re always on the lookout to anticipate market forces that aren’t the focus of mainstream media’s daily ebb and flow and SPEAR’s investment strategy is sound and consistent in our view.

As always, like Ivana Delevska, do your own homework and come to your own conclusions. We hope our data and input can be a useful source.

Keep in Touch

Many thanks Ivana Delevska for her insights and contributions for this episode. Alex Myerson and Ken Shifman are on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Image: Rudzhan

Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.