Despite fears of inflation, supply chain issues, skyrocketing energy and home prices and global instability caused by the Ukraine crisis, CIOs and IT buyers continue to expect overall spending to increase more than 6% in 2022. While this is lower than our 8% prediction made in January of this year, it remains in line with last year’s roughly 6-7% growth and is holding firm with the expectations reported by tech executives last quarter.

In this Breaking Analysis we update you on our latest look at tech spending with a preliminary take from ETR’s latest macro drill down survey. We’ll share some insights as to which vendors have shown the biggest change in spending trajectory and ask the technical analysts in our community to give us a read on what they think it means for technology stocks going forward.

The spending sentiment among IT buyers remains solid

In the past two months we’ve had conversations with dozens of CIOs, CDOs, data executives, IT managers and application developers. Across the board they’ve indicated that, for now at least, their spending levels remain largely unchanged. The latest ETR drill down data, which we’ll share shortly, confirms these anecdotal checks.

However the interpretation of this data is nuanced. Part of the reason for the spending levels are holding up is inflation. Stuff costs more so spending levels are higher, forcing IT managers to prioritize. Security remains the #1 priority and is less susceptible to cuts. Cloud migration, productivity initiatives and data projects remain top priorities.

So where are CIOs robbing from Peter to pay Paul? We’ve seen a slight uptick in certain speculative IT projects being put on hold and according to ETR survey data, we’ve seen some hiring freezes reported, especially notable in the healthcare sector.

Vendor Consolidation is the Most Cited Savings Tactic

ETR also surveyed its buyer base to find out where they were adjusting their budgets. Consolidating IT vendors was by far the most cited tactic. This makes sense as companies, in an effort to negotiate better deals, will often forgo investments in newer best of breed technologies and bundle in products and services from larger suppliers, even though they may not be as functional.

ETR survey respondents also cited cutting the cloud bill where discretionary spending was in play. We certainly saw this with some of the largest Snowflake customers this past quarter where even though they were still growing consumption rapidly, certain customers dialed down their consumption and pushed spending off to future quarters. Remember, in the case of Snowflake anyway, customers negotiate consumption rates based on a total commitment over a period of time. So while they may consume less in one quarter, over the lifetime of the contract, Snowflake (and several other cloud companies) have good visibility on the lifetime value of a deal.

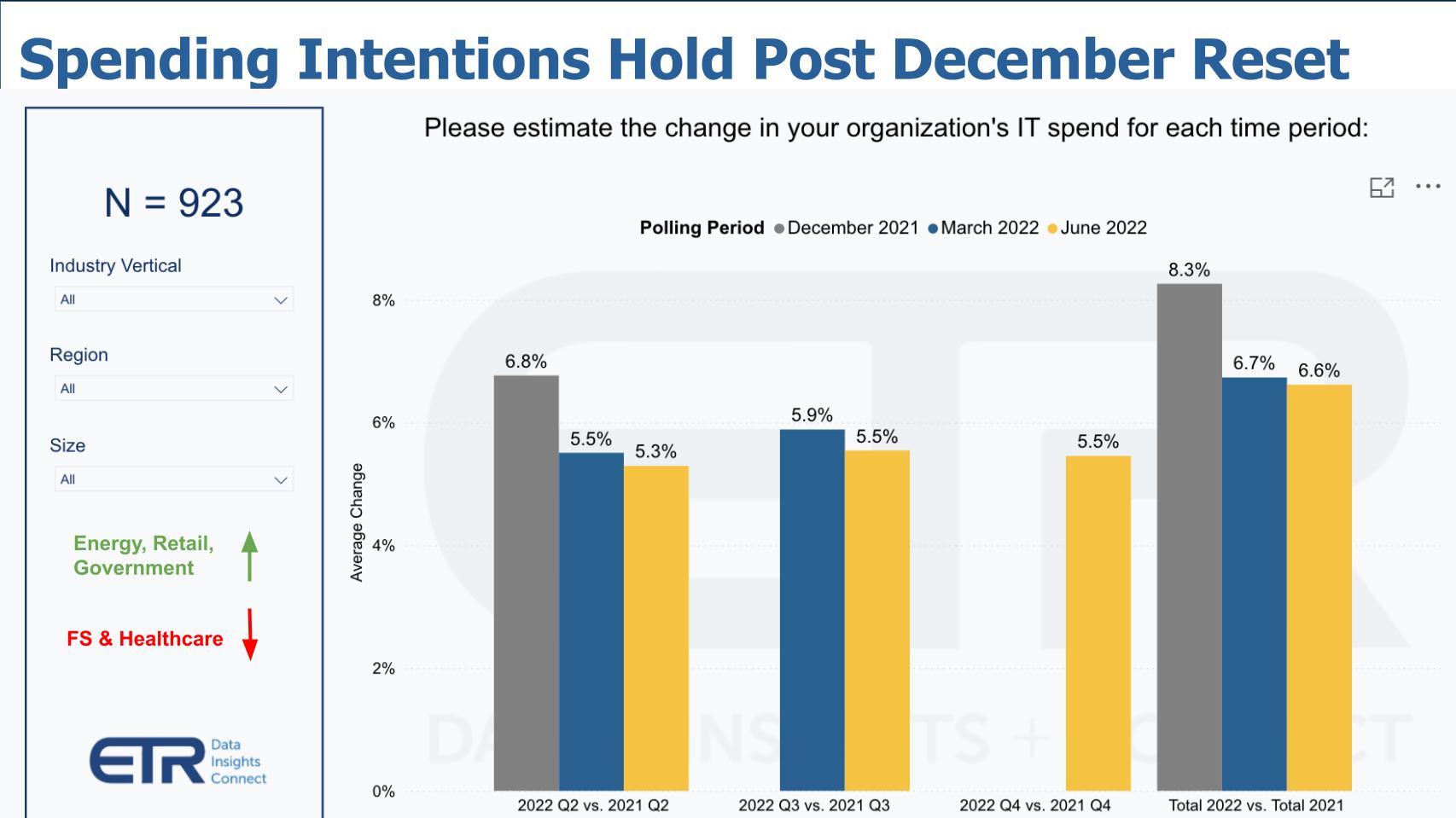

Buyers Expect Spending Levels to Remain Stable (for Now)

The chart above shows the latest ETR spending expectations among more than 900 respondents. The bars represent spending growth expectations from the periods of December 2021 (gray bars); the March of 2022 survey (blue); and the most recent June data (yellow).

You can see the expectation for spending in the quarter is down slightly in the mid 5% range but overall for the year, expectations remain in the mid 6% levels. This figure is down from 8%+ in December, where it looked like 2022 was going to have more momentum than even last year. Remember this was before Russia invaded Ukraine which occurred in mid February of this year.

Generally speaking, CIOs have told us that their CFOs have lowered their earnings outlooks for Wall Street. They’ve told us that unless and until these revised forecasts appear at risk, they continue to expect their spending levels to remain pretty constant.

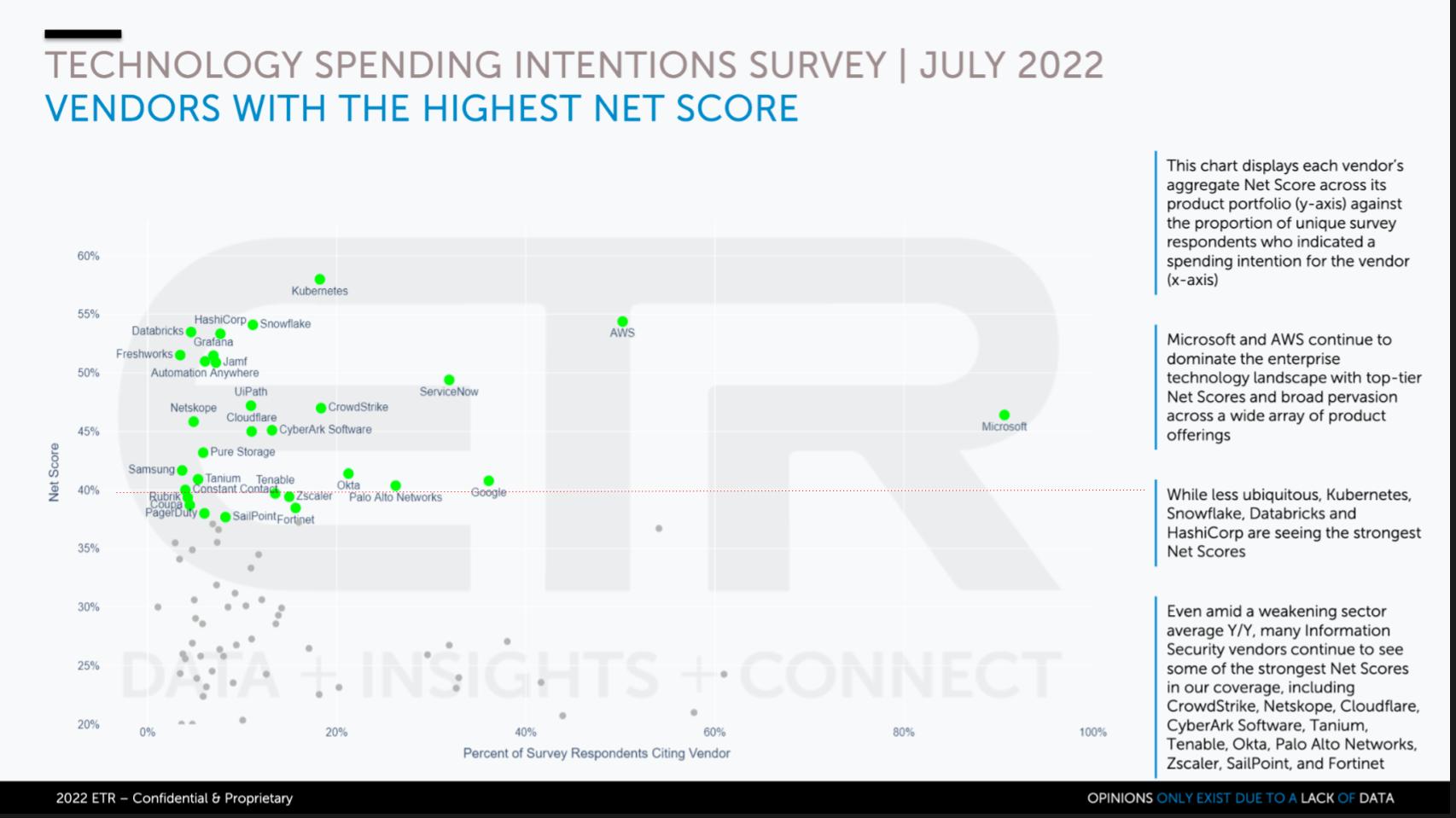

Plenty of Spending Momentum on Specific Vendor Platforms – Security Co’s Lead the Pack

The chart above shows the companies with the greatest spending momentum as measured by ETRs proprietary Net Score methodology. Net Score measures the net % of customers spending more on a particular platform. That measurement is shown on the Y axis. The red line inserted at 40% is a highly elevated marker and the green dots are companies in the ETR survey that are near or above that line. The X axis measures the presence or pervasiveness in the data set.

Now of course, Kubernetes is not a company but it remains an area where organizations are spending lots of resources and time – particularly to modernize and mobilize applications. Snowflake remains the company which leads all firms in spending velocity but as you’ll see momentarily, despite its highest position it’s down from previous levels in the high 70’s and low 80% range.

AWS is incredibly impressive because it has an elevated level but also a huge presence in the survey. Same with Microsoft. Same with ServiceNow which stands out. And you can see the other smaller vendors like HashiCorp, which is increasingly being seen as a cross-cloud enabler, showing elevated spending momentum. The RPA vendors, Automation Anywhere and UiPath are in elevated territory. But it’s the security companies that really standout. Crowdstrike, CyberArk, Netskope, Cloudflare, Tenable, Okta, Zscaler, Palo Alto, Sailpoint, Fortinet are all showing elevated levels with many cybersecurity firms hovering at or above the 40% mark.

Pure Storage remains elevated as do Pagerduty and Coupa.

There’s plenty of good news here despite the tech crash.

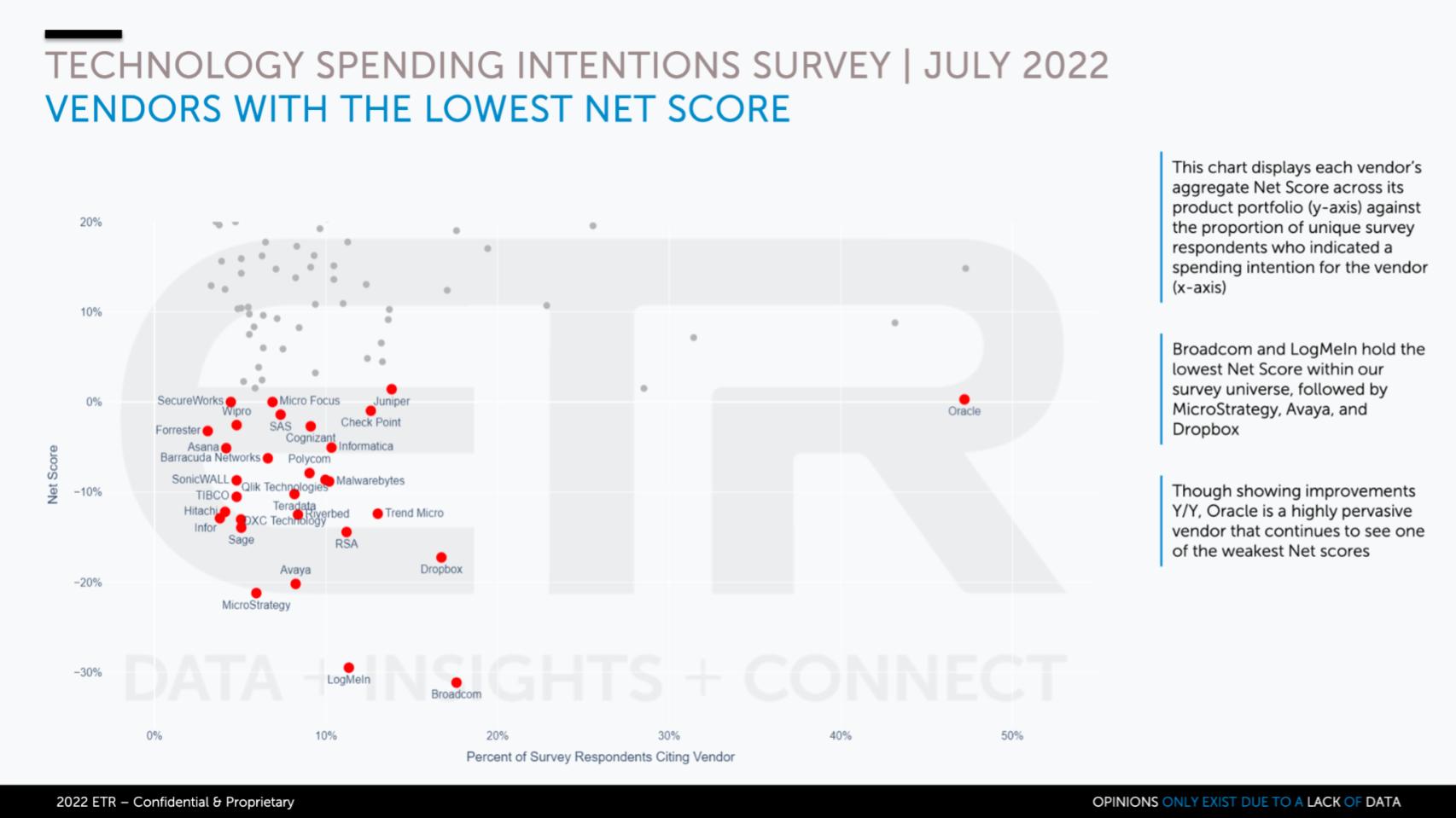

Now for the Red Team

There is no 40% line on the above chart because all these companies are well below that line. Now this doesn’t mean these companies are bad companies. It just means that a higher number of companies in the ETR survey are spending less than more on the particular company’s products and services. In other words, they don’t have the spending velocity of the ones we showed earlier.

A good example is Oracle – look how they stand out on the X axis with a huge market presence. Despite its lower Net Score, Oracle remains an incredibly successful company selling to high end customers and owning the mission critical data and applications markets. And remember, ETR measures spending activity but not actual dollars. So companies like Oracle, with big budget customers are not rewarded in the ETR surveys. Nonetheless, the fact remains that Oracle has a large legacy installed base that pulls down its growth rates, which ETR does capture.

Broadcom is another example. They’re one of the most successful companies in the industry. They’re not going after growth at all costs. They’re going after EBITDA, which ETR doesn’t measure.

So just keep that in mind as you look at this data.

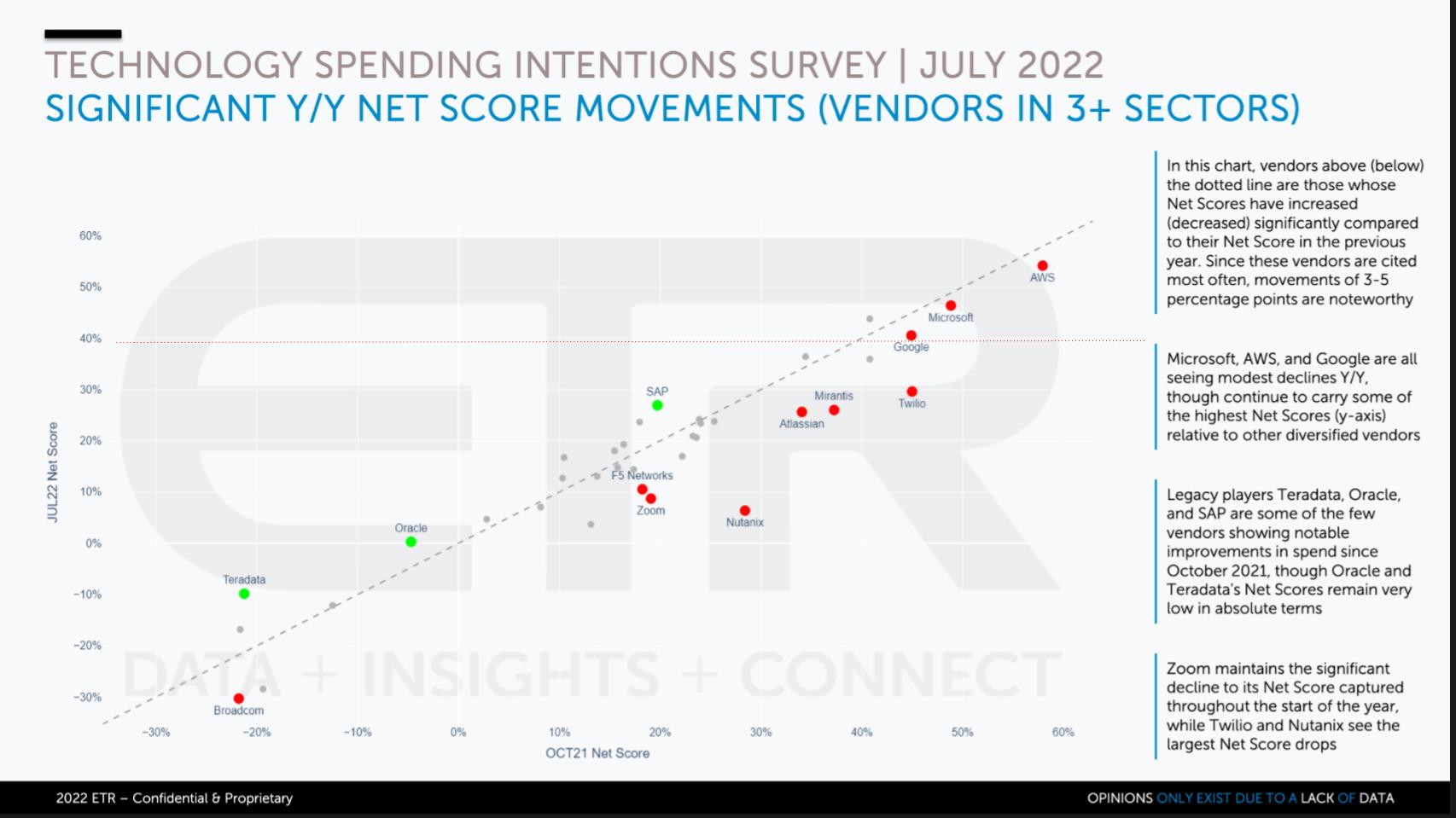

How is Spending Velocity Changing Over Time?

The chart above shows the year over year Net Score change for vendors that participate in at least three sectors within the ETR taxonomy. Names above or below the gray dotted line are those companies where the Net Score has increased or decreased.

Putting this in context with the earlier chart, it’s all relative right? Oracle, while having lower Net Scores has also shown a more meaningful improvement than some of the others, as have SAP and Teradata.

What’s impressive here is how AWS, Microsoft and Google are actually holding the line pretty well. The other ironically interesting two data points here are Broadcom and Nutanix. Broadcom is buying VMware and of course most customers are concerned about getting hit with higher prices. Nutanix, despite its change in Net Score, is in a good position to capture some of that VMware business. Just yesterday we talked to a customer who told us he migrated his entire portfolio off VMware, using Nutanix AHV in an effort to avoid the V-Tax. Now this was a smaller customer and not representative of what we believe is Broadcom’s ICP – ideal customer profile…but Nutanix should benefit from the Broadcom acquisition if it can position itself to pick up the business Broadcom doesn’t want.

One person’s trash is another’s treasure…

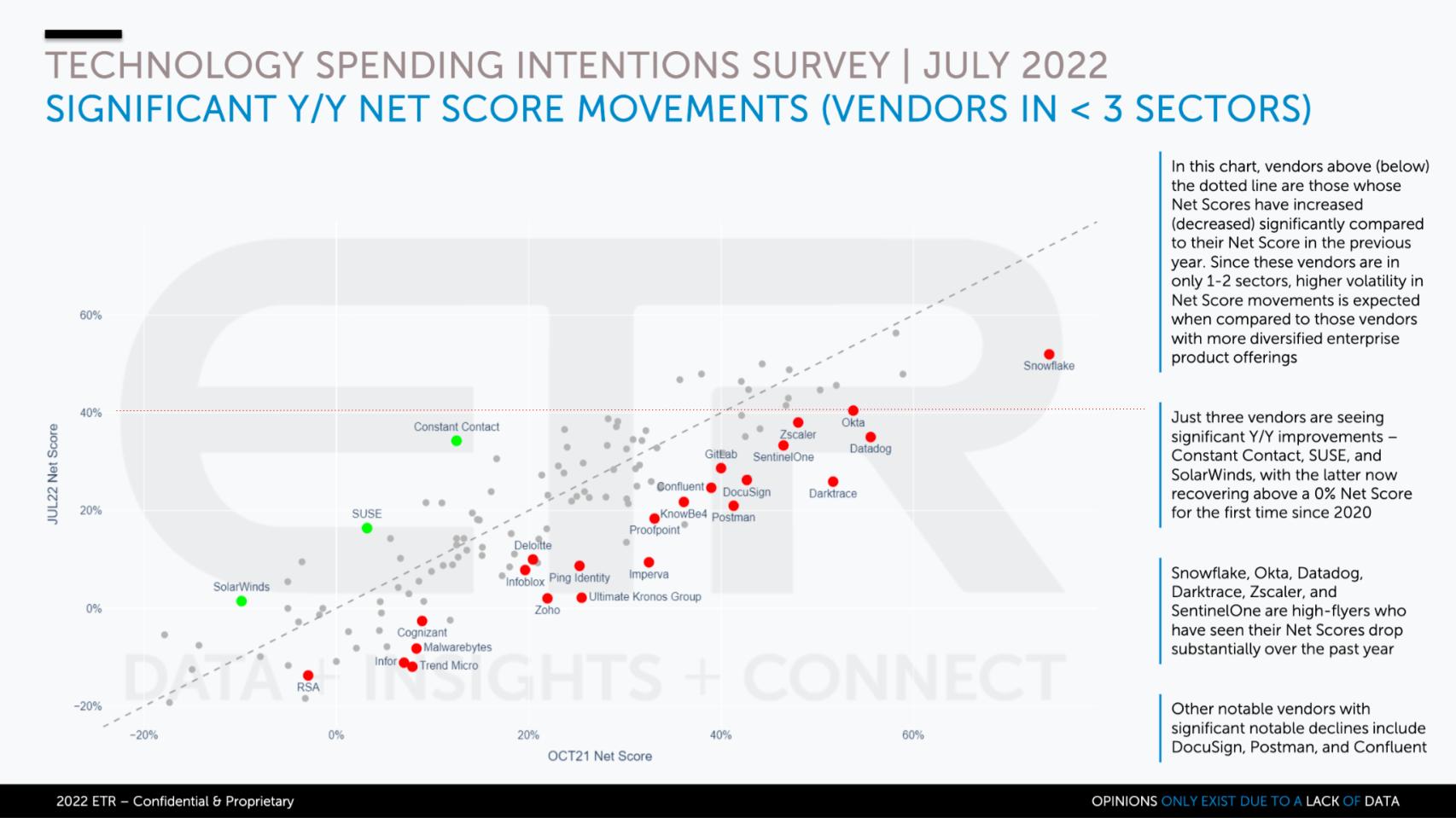

Change in Spending Velocity for ‘Pure Play’ Companies

Above is the same chart as the previous one for companies that participate in two or fewer segments within the ETR taxonomy.

Only three names are seeing positive movement year over year in Net Score. SUSE, under the energizing leadership of Melissa Di Donato is making moves. It went public last year and acquired Rancher Labs in 2020. We know Red Hat is the big dog in Kubernetes but since the IBM acquisition, people have looked to SUSE as a potential alternative and it’s showing in the numbers. SUSE has a nice business and will do more than $600M in revenue this year with solid double digit growth. Its profitability is under pressure but they’re definitely a player that has found a niche and is worth watching.

Solarwinds is maybe a bit of a dead cat bounce coming off the major breach – some of its customers just can’t move off the platform.

In that sea of red dots there are many high PE stocks – or infinite PE stocks that have no E – and we can see how their Net Scores have dropped. We’ve reported extensively on Snowflake – still #1 in Net Score but big moves off their highs. Okta, Datadog, Zscaler, SentinelOne and Dynatrace all showing big downward moves along with the rest. So this chart really speaks to the change in expectations from the COVID bubble, despite the fact that many of these company’s CFOs would tell you the pandemic wasn’t necessarily a tailwind for them.

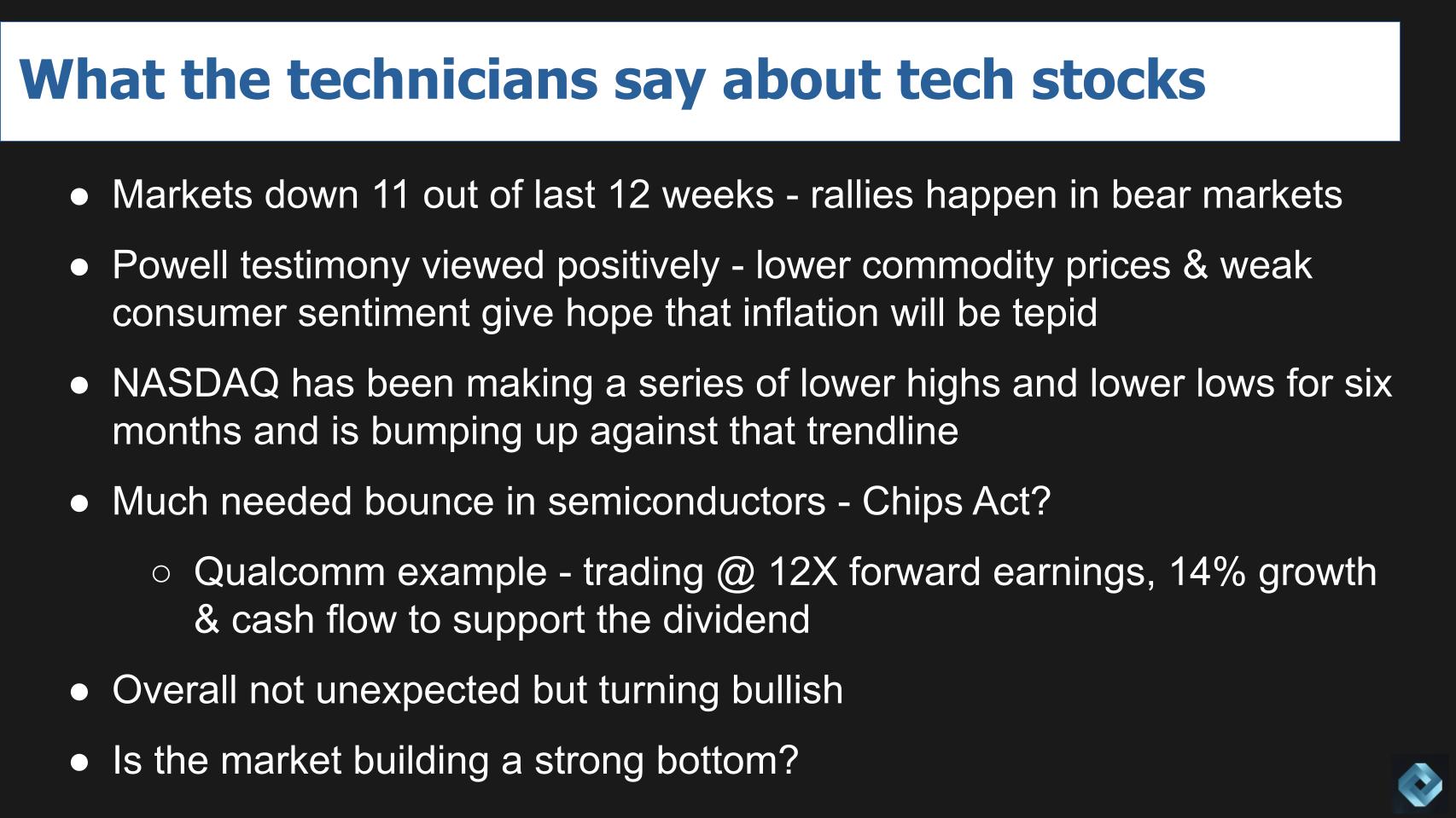

Bear Market Rally, Time to Buy or Building a Base – What do the Technicians Think?

The big question on people’s minds is what’s going to happen to these tech companies in the stock market?

We reached out to both Erik Bradley of ETR, who used to be a technical analyst on Wall Street. We also talked to long time trader and frequent Breaking Analysis contributor Chip Symington to get a read on what they thought.

The first observation is the market has been off eleven out of the past twelve weeks and bear market rallies like what we’re seeing today happen from time to time.

Chair Powell’s testimony was viewed positively by the street because higher interest rates are expected to push commodity prices down and weaken consumer sentiment, which may point to a less onerous inflation outlook.

Symington pointed out to Breaking Analysis a while ago that the Nasdaq index has been on a trendline for the past six months where its highs are lower and the lows are lower and we’re bumping up against that trendline at these levels. What he means is if it breaks that trend it could be a buying signal as he feels that tech stocks are oversold.

He pointed to a recent and much needed bounce in semiconductors and cited the Qualcomm example. Here’s a company trading at 12X forward earnings with a sustained 14% growth rate and cash flow to support its 2.42% annual dividend.

So overall he feels this rally was expected. He’s cautious because we’re still in a bear market but he’s beginning to turn bullish.

Erik Bradley added that he feels the market is building a base here and he doesn’t expect a 1970’s/80’s yearlong sideways move because of all the money that’s still in the system. But it could bounce around for several months and with higher interest rates, there will be more options other than equities, which for many years hasn’t been the case.

Obviously inflation and recession are like two looming towers that we’re all watching closely and will ultimately determine if, when and how this market turns around.

As always, we’ll be here watching the data and reporting material changes to our community.

Keep in Touch

Thanks to Stephanie Chan who researches topics for this Breaking Analysis. Alex Myerson is on production, the podcasts and media workflows. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE. And special thanks this week to Andrew Frick, Steven Conti, Anderson Hill, Sara Kinney and the entire Palo Alto team.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.