Premise: After many years of build-out, both in terms of data centers and on-demand services, the public cloud market is finally becoming more competitive. As Amazon AWS moves into a new stage of financial transparency, Microsoft Azure has turned the corner and now has competitive, compelling offerings for both developers and Enterprise IT. These heavyweights have the resources and offerings to define the playing field for the next decade.

Stu Miniman (@stu) and Brian Gracely (@bgracely) previewed the upcoming AWS re:Invent 2015 conference (watch full coverage on theCUBE), as well as discussing the shifting landscape in Public Cloud.

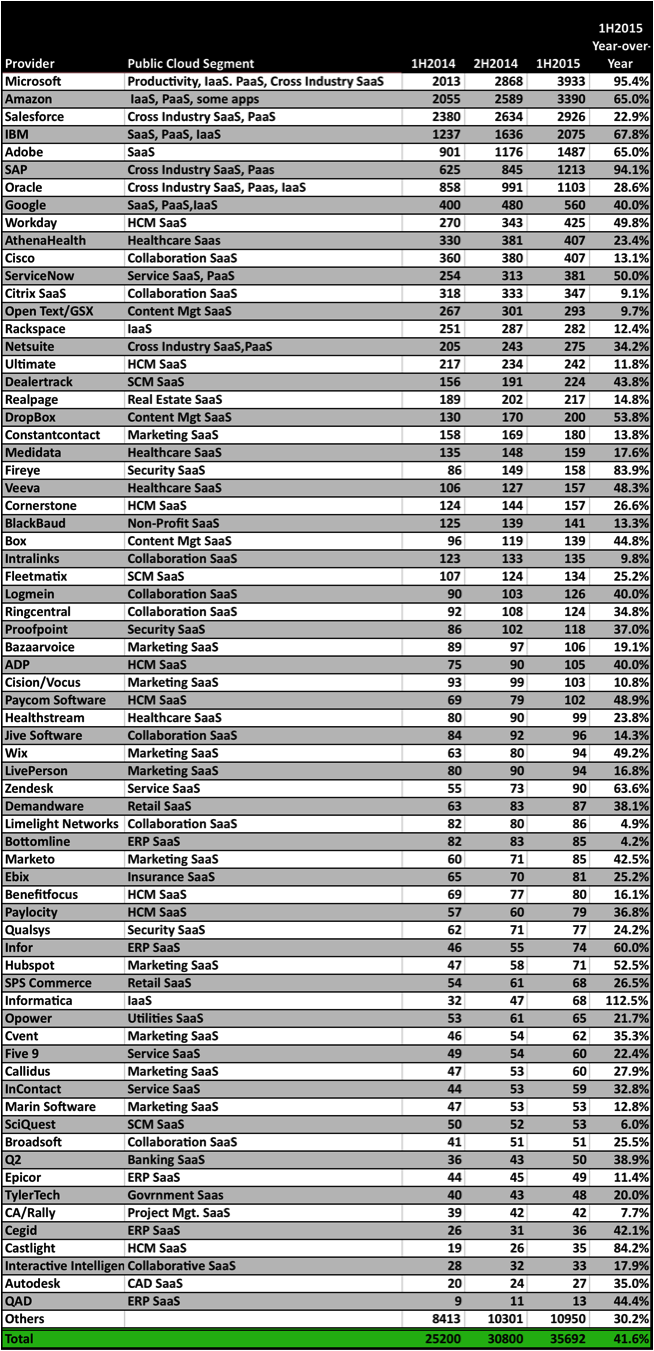

When Wikibon published the Public Cloud Market Shares (2014-2015) and subsequent market forecast for Public Cloud (2015-2026), many people took a short-term view and wanted to question the methodology used or the granularity of the results. Was it fair to include O365 in the Microsoft numbers given the massive installed base on Microsoft Office on end-user devices? Pundits can debate the nuances of those details, hopefully with more specificity as the hyperscale cloud providers continue to add transparency to their reporting. But several things that can not longer be debated are:

[1] Public Cloud and the on-demand economic models are legitimate threats to Enterprise vendors

[2] Public Clouds are a viable alternative for Enterprise IT customers

[3] The competitive landscape for Public Cloud is beginning to become clearer in terms of where each company will primarily focus and where certain battle lines are being drawn.

Public Cloud Market Leaders IH’14, 2H’14, 1H’15 and Year-over-Year Growth Rates

Evolving Public Cloud Strategies

While every Public Cloud provider offers a set of infrastructure services and some higher-level application services, their individual strategies and strengths are beginning to evolve and become more visible. Given these advancement in the breadth of cloud services, it is expected that we will begin to see a large percentage of end-user customers using multiple Public Cloud providers. In some cases, this may be their “Hybrid Cloud”, especially if many of their legacy applications do not require the agility of a scalable cloud-based private environment.

Amazon AWS – The Developers Choice

For many years, Amazon’s AWS defined not only the possibilities of the Public Cloud market, but also the developer-experiences and developer-expectations. In that way, they were like that BASF commercial – AWS didn’t make the SaaS applications, they made them better. As AWS evolved, so too did the economics of VC funding. Instead of funding for Innovation + CAPEX, 1000s of startups are now funded for Innovation + OPEX, with the default OPEX being AWS. AWS appealed to the developers that either had no legacy IT, or to the developers that were frustrated with legacy IT. Their architecture appealed to the developer mindset by offerings lots of tools/services that allowed developers to pick and choose what worked best for them. While AWS has aggressively hired sales and marketing to attack a broader segment of the Enterprise market and move upstream into more application-centric services, this next stage of growth could be more complicated. AWS will be fighting friction more than enabling innovation, which can lead to longer lead cycles and more demand for features/services that generate less headlines – but often more revenues.

Microsoft Azure – Hybrid for the Enterprise

It’s never easy to transition a business, let alone one of the largest businesses in the world. The tech graveyard is filled with companies that tried to pivot and have failed. For many years, Microsoft looked like it was becoming over of those companies that wouldn’t be able to transition away from their entrenched businesses of Windows and Office on PCs. But as new leadership evolves, times are quickly changing in Redmond. Linux is being embraced. A minimal Window OS (Nano Server) is being embraced. And Microsoft Azure has done a 180* turn from the early struggles with PaaS on Azure. With the AzureConf announcements yesterday, Azure’s strategy is becoming more well defined. While it is getting closer to AWS portfolio of cloud services for modern application developers, it is also playing to its strengths with existing IT organizations. Azure can leverage the installed based on Windows Server to enable a Hybrid Cloud strategy, for those customers that aren’t moving towards an “All In” strategy in the public cloud. Add to this a growing set of services for SQL databases and Enterprise-friendly pricing models, and Microsoft Azure’s strategy is less about revolution and disruption as it is about evolution for Enterprise businesses.

IBM Cloud – Managing Complexity for the F500

Back in the 1940s, Thomas J. Watson claimed that, “there would would only be a world market for 5 computers”. Given the massive size of Public Cloud providers, his prediction eventually be right; in a cloud sense. IBM has been evolving their cloud strategy through a series of acquisitions (e.g. Softlayer, Bluebox , internal development (e.g. Watson) and open-source community activities (e.g. BlueMix). Early investment in understanding and contributing to open-source communities is beginning to pay dividends as the BlueMix strategy is heavily influenced by open-source projects such as OpenStack, Docker and Cloud Foundry, as well as deep involvement from IBM in Linux communities. IBM has always been strong in Multi-National and F500 companies, but they are now beginning to add offers that could tap into SMB markets. IBM’s strategy is evolving into a set of managed services, targeting modern and complex technologies that many companies are not able to staff or train for internally.

Google Cloud Platform – Focused on Analytics and Verticals

Of the four global hyperscale cloud providers, Google Cloud Platform’s strategy has been the most confusing to follow and anticipate. While nobody doubts Google’s experience and scale in operating cloud-based services, their business-centric offerings and execution have left many people to wonder if Google Cloud Platform will someday join the ranks of other Google projects that just went away or got ignored (e.g. Google Wave, Google Buzz, Google Plus). While Google does continue to release infrastructure-centric services, they are beginning to focus more of their strategy on analytics solutions and vertical-market solutions (e.g. Healthcare, Media & Entertainment, etc.). This is where Google’s global network and deep expertise in data can be differentiated to customers.

Too Big to Fail?

The Public Cloud discussion is often dominated by the four large cloud providers (AWS, Azure, IBM and Google), but what about the others? From a longevity perspective, the first question to ask is if smaller providers can compete with the economies of scale of the big 4. This is where HP Helion Cloud, VMware vCloud, EMC Virtustream and Digital Ocean are attempting to carve out a niche based on application-specific offerings or interoperability. The next question to ask is if network footprint (eg. CenturyLink Cloud) will eventually be a critical factor, as telcos and cable companies have extensive presence but have yet to build large cloud businesses (to date). And the final question to ask if if geographic presence will become a bigger issue as data sovereignty issues become a bigger concern outside the United States. With the expected growth of the Internet of Things and Industrial Internet, proximity to cloud data centers will eventually play a more critical role to end-customers.

Eight years into the IaaS evolution and the market has seen both explosive growth and market consolidation. It has lead to the rapid rise of the SaaS market and the emergence of the PaaS market. Wikibon believes that we’re in the beginning stages of the 2nd phase of the evolution of Public Cloud, with huge new opportunities emerging around Mobile, Analytics and IoT.

Action Item: Customers have more choices than ever to begin leveraging Public Cloud services to solve their business challenges. The market continues to growth at a rapid pace and the offerings are beginning to differentiate themselves across the cloud providers. Businesses that don’t have a well-defined Public Cloud strategy and are executing new projects in this domain will find themselves in a competitive disadvantage in the next 12-18 months.