Contributing Wikibon Analysts

David Floyer

Brian Gracely

Stu Miniman

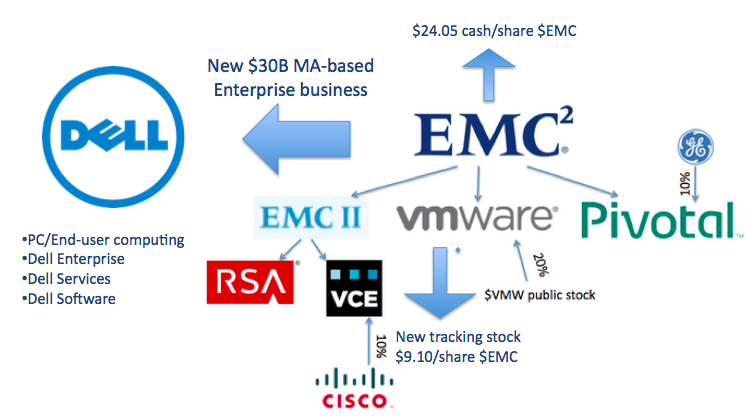

- The Numbers: Dell announced it is acquiring EMC for approximately $67B – the math works like this…EMC shareholders get:

a. $33.15 per share comprised of:

i. $24.05 per share in cash which equates to about $49B

ii. $9.10 per share in the form of a VMware tracking stock – worth approximately $18B in value

b. EMC currently owns about 81% of VMware’s shares while the public market currently owns about 19% (including about a 4% ownership by Cisco). Post transaction, Dell/Silver Lake/MSD Partners/Denali Holdings will continue to control 81% of VMware’s voting shares and because of the tracking stock, it will maintain somewhere around 28% of VMware’s outstanding stock value.

- The Timing: The transaction will complete sometime between May and October 2016. Regarding layoffs, while Dell didn’t commit to no workforce reductions, Joe Tucci indicated nothing would happen until next summer.

- The ROI: Dell is promising within 18-24 months it will de-leverage (i.e. pay down its debt). How do companies manage cash cows? Answer – they leverage their lockin: 1) Longer product cycles; 2) Increase maintenance/support costs; 3) Cut salaries; 4) Narrow the R&D focus; 5) Charge a premium – We expect this to be the likely Dell playbook for VMAX, VNX, Data Domain, Compellent, etc.

- Growth? To enable de-leveraging, Dell and EMC cited that revenue synergies will be 3X cost synergies. There isn’t much overlap in business lines between Dell and EMC so the cost synergies are somewhat limited – and revenue synergies take time to create. There will be revenue synergies from VMware differentiation (i.e. EMC’s playbook for years), however that dynamic has the tendency to constrict VMware’s growth and ecosystem options. The obvious areas of synergy are to: 1/ drive Dell server content into EMC products, especially converged infrastructure, 2/ Pump products through Dell’s channels and 3/ Use EMC’s deep relationships in large accounts to upsell end-to-end mobile, laptop, servers, storage, VMware and services.

- $30B Enterprise Business – Michael Dell indicated he would create a $30B enterprise business that would be run out of Massachusetts. This would likely include EMC + Dell Servers + Dell enterprise storage. No announcement was made as to whom will run this business but we would expect David Goulden would receive that position.

- Whither the Cisco Relationship – Dell and EMC have said that the VCE partnership will remain intact. About 20% of Cisco’s UCS business comes from VCE or about $600M. Dell will eye this business and we believe try to vertically integrate to capture a portion of that revenue. On the flip side, Dell doesn’t really have the high-end blade server presence that Cisco has, or the high-end networking assets. As well, VCE generates $2B per annum in revenue, so there’s no way Dell and EMC will throw that business away. Expect Dell to walk a fine line with Cisco, preserving the relationship as long as reasonably possible, keeping seams in the portfolio tight (expect more overlap than gaps) while at the same time, creating new converged infrastructure solutions with Dell servers and networking.

- The New Monster – The combined EMC and Dell will be a roughly $75-$80B entity and look something like this:

a. Dell PCs/End User Computing ~$28B

b. Dell Enterprise ~$13B

c. Dell Services ~$8B

d. Dell Software ~$1B

e. EMC Storage ~ $17B

f. VMware ~ $6B

g. RSA ~ $1B

h. Other ~1B (Pivotal, Content Management)

Source: Wikibon, 2015

- Margin Mania – Dell has managed low margin businesses successfully and is well positioned to do the dirty work of streamlining EMC to compete in the marketplace. Dell’s gross margin has hovered for years in the high teens/low 20’s whereas EMC sees gross margin in the 60’s. Our estimates indicate that the combined entity will have gross margins in the 35% range, significantly higher than Dell’s current business model. As such, EMC will lift Dell’s fundamental profit model in the short-term. A key long-term issue will be the degree to which Dell allows VMware to “take off the gloves” and compete in the $35B storage business with its software-defined strategy. The strategy, in our view, will be to lower prices, gain share and do so at lower margins while maintaining profitability. Michael Dell stated that public markets are helpful for high growth companies that need cash; Dell and EMC throw off cash and can manage (slower) growth without the need for public equity.

- The Gestalt – This deal underscores the broader move toward the public cloud and the impact of open source on challenging traditional enterprise lock-in models. Linux running storage and apps and the corresponding ecosystems, combined with the ascendency of new data storage models running in the cloud are creating “hard times in hard-ware.” The industry structure is shifting toward organizations that are leveraging an increasingly capable “Digital Matrix” that supports transformations to a so-called Digital Economy. EMC is increasingly under pressure from this transition. Joe Tucci is fond of invoking the “Waves of Change” analogy, where some companies don’t make it through subsequent transitions. The waves appear to be too gnarly for EMC to go it alone.

a. Looking at several major disruptions and EMC’s contribution as measured by share and impact:

a. Mobile: Negative

b. Public Cloud: Negative

c. Big Data: Neutral

d. Social Media: Negative

e. Flash: Positive

f. Open Source: Negative

g. Convergence: Positive

h. Hyperconvergence: Negative

i. IoT: TBD

j. Systems of Intelligence: TBD

- Another White Knight is Doubtful – This deal is not closed yet. EMC reportedly negotiated a “Go Shop” provision with a reduced breakup fee if EMC sells to another bidder (reportedly $2.5B to Dell’s reported $6B termination fee). As well there’s a collar on the deal that protects both parties from large fluctuations in EMC’s stock price. Given the premium EMC is receiving (about 33% since its October 2, 2015 closing price), it’s unlikely other suitors will come to the table. Reports have IBM (not likely), Oracle (slim to no chance), HP (already passed) and Cisco as possible suitors. Of these Cisco is the most interesting but we believe management has its sites set on IoT, not being a steward of infrastructure consolidation.

Note: HP’s Meg Whitman issued an internal memo stressing that Dell will carry a $2.5B annual debt service with this deal. We don’t see this as problematic if Dell can quickly de-leverage by cutting costs and finding revenue opportunities. Both Dell and EMC are excellent M&A operators and the $2.5B annual nut is in the range of what the combined Dell/EMC would spend on acquisitions each year. For the time being, the new company will be focused on integration and paying down the debt and not acquiring companies.

While we are concerned about the creation of a new industry giant, and generally are not enthusiastic about such deals (as they tend to reduce competition for customers), from Dell’s perspective it accelerates Michael Dell’s enterprise vision. We think he and Silver Lake will profit. We also believe something like this was necessary as we never felt EMC was well-positioned against Amazon specifically and the public cloud generally.

For EMC’s part we’re publicly disappointed that the end to its legacy came this way. Make no mistake– despite the spin, EMC as we know it – the customer-centric, high margin, never give up and win at any cost storage champion will be gone forever.

Finally– we’ll be closely watching what happens with VMware. Will Dell sell the asset or try to vertically integrate and dominate the hardware and software infrastructure business — end to end. We believe what Dell does with VMware will determine the pace of ecosystem defection and/or loyalty and have meaningful impacts on the outcomes within enterprise IT.

Action Item: Join the #DellEMC CrowdChat and watch theCUBE next week from Dell World as Michael Dell joins us to add further insight to the deal.