Cisco is a company at the crossroads. It is transitioning from a high margin hardware business to a software subscription-based model through both organic moves and targeted acquisitions. It’s doing so in the context of massive macro shifts to digital and the cloud. We believe Cisco’s dominant position in networking, combined with a large market opportunity and a strong track record of earning customer trust, put the company in a good position to capitalize on cloud momentum. But there are clear challenges ahead, not the least of which is the growing complexity of Cisco’s portfolio, transitioning a large legacy business and the mandate to maintain its higher profitability profile as it moves to a new business model.

In this Breaking Analysis, we welcome in Zeus Kerravala, Founder and Principal Analyst at ZK Research and long time Cisco watcher who collaborated with us to craft the premise of this session. As always, we’ll look at survey data from Enterprise Technology Research and provide our analysis of what it means for Cisco and the broader industry.

Catalyst – Cisco’s Investor Day

The genesis for this session was we attended Cisco’s financial analyst day and received a day and half firehose of presentations, drill-downs and interactions with key Cisco executives and a customer.

We’re going to share our takeaways from these sessions and add our additional thoughts. In particular we’re going to discuss how Cisco views its TAM, the company’s transformation to a subscription-based model and how we see that evolving in the context of industry dynamics.

As always, we’ll bring in some ETR spending data for context and get Zeus’ take on what it tells us. And we’ll end with a summary of Cisco’s cloud strategy and outlook for how it can win in the cloud.

Understanding Chuck Robbins’ Organization

A little over a year ago, after the departure of EVP David Goeckeler, Cisco’s CEO made moves to flatten the organization by both promoting from within and bringing in some outside talent. The company’s executive leadership team (ELT) comprises the requisite finance, admin, HR, comms, legal and policy executives.

Cisco’s product groups are organized around logical technology areas but it’s sometimes difficult to map products to how Cisco goes to market. Generally the technology/product groups are organized around network equipment (Todd Nightingale), service provider routing (Jonathan Davidson), datacenter offerings/aka applications (Liz Centoni), collaboration & security (Jeetu Patel), silicon & optics (Eyal Dagan) and services (Maria Martinez). These execs often have additional cross-functional responsibilities – e.g. Liz Centoni is also the Chief Strategy Officer…Maria Martinez is the COO title.

Zeus Kerravala explained the organization as follows:

The ELT is organized around product roadmap and product innovation, but that’s not necessarily the way customers purchase things. Cisco used to report to the street three product segments: 1) infrastructure platforms, which was by far the biggest, it was all their networking equipment; 2) then applications, and 3) security. Now it’s moved to five new segments, secure agile networks, hybrid work, end to end security, internet for the future and optimized app experiences. And I think what Cisco’s trying to do is align the way they report to the way customers buy.

How Cisco Thinks About its TAM

One of the big takeaways at the investor meeting was how Cisco sees its total available market. Liz Centoni and CFO Scott Herren showed the following slide.

The message was that Cisco has a large and growing market and a TAM of somewhere between $800 and $900B depending on which slide and data points you use. The point is Cisco is not constrained by lack of opportunity.

Zeus Kerravala gave his thoughts on Cisco’s TAM expansion strategy as follows:

The big takeaway from the data is there’s still a lot of room ahead for Cisco to grow. It’s a company most people would put in the camp of legacy IT vendor, just because of how long they’ve been around. But they have done a very good job of innovating. And part of that is just these markets that they play in continue to grow and customers continue to have challenges that Cisco can solve. One of the things Cisco has done since the arrival of Chuck Robbins is they don’t fight these trends anymore. Prior to Chuck’s arrival, they resisted the tide of software defined networking and trends like cloud to some extent. I remember one of the first meetings I had with Chuck, I asked him about that and he said that Cisco will never do that again. That under his watch, if customers are going through a market transition, Cisco wants to lead them through it, not try and hold them back. And I think for that reason, they’re able to look at all of those trends and try and take a leadership position in them, even though some of them might be detrimental to Cisco’s business in the short term. For example, something like software defined WANs, which you would throw into secure agile networks, may not carry the same kind of RPOs and margins with it that their traditional routers did, but ultimately customers are going to buy it and Cisco would like to be the ones to sell it to them.

Transition to a Subscription-based Model

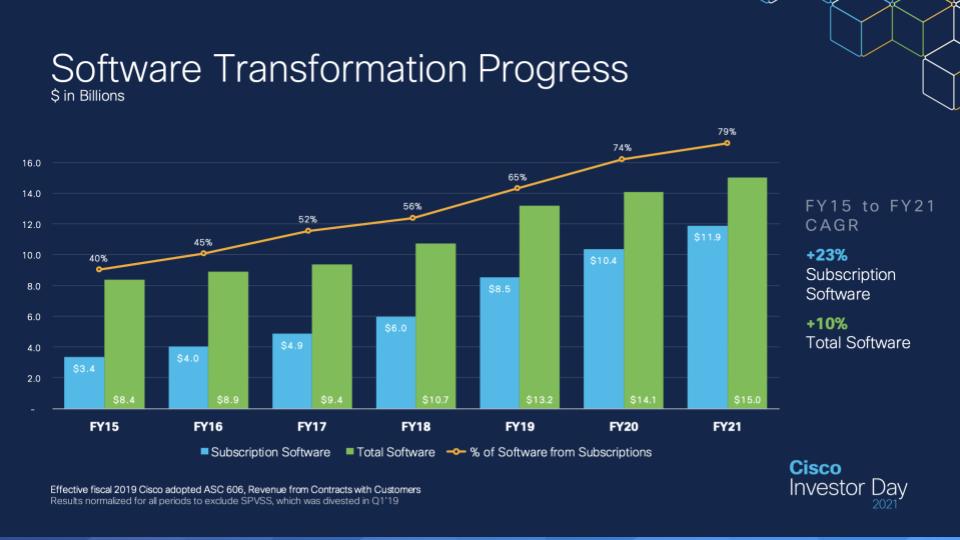

The other big takeaway was the shift to software and subscription revenue. Below is a chart Cisco showed to make the point that it’s one of the largest software companies in the world – certainly within the top 10.

Cisco also stressed since Chuck Robbins became CEO in 2015, it has nearly 4X’d its subscription software revenue and roughly doubled its overall software sales. And it has an RPO (remaining performance obligations) that exceeds $30B. It’s also committing to grow its subscription business by 15-17%, CAGR through FY 2025, which would imply a doubling of the blue lines to more than $20B

That forward looking forecast likely includes some services that become bundled into subscriptions, the same way SaaS companies report. But the point is Cisco is committed, like many of its peers, to moving toward an ARR (annual recurring revenue) model.

Zeus Kerravala stressed the following points:

- This is a massive shift for Cisco and one that is disruptive, not only to Cisco but also the channel due to the shift away from a big up front revenue recognition hit;

- It dramatically changes the way you deal with the customer. When you sell a one-time product, you basically wipe your hands and come back in three or four years to say, ‘it’s time to upgrade.’ When you sell a subscription, it becomes incumbent on the partner and Cisco to make sure that customer is adopting and renewing.

- Cisco’s pure software business – e.g. in collaboration and parts of its security portfolio – can make this transition much more easily. The traditional networking equipment transition to ARR will be much more challenging.

On-prem As-a-Service Pricing is Table Stakes

Virtually every legacy hardware company has announced plans to move to consumption-based pricing. HPE is all in with GreenLake, Dell has made APEX a priority, IBM has its version as do Lenovo and Cisco with Cisco Plus. Oracle was actually one of the first to implement such a model with its Cloud at Customer offering. We feel the following observations are important to highlight:

- Generally we see these moves as necessary but insufficient for winning the day in cloud. These programs have typically evolved from service-led, financing models and are five years late in coming to market in our view;

- We believe they’re largely a defensive response to the threat from cloud and a trend on Wall Street to reward predictable ARR models;

- Most of these programs are vendor-centric, designed to preserve revenue and margins while appearing to give customers cloud-like flexibility. They are not true cloud-like consumption-based models in that they require customers to make a minimum commitment for a term regardless of consumption patterns. You can’t ever shut off the one-way payment spigot like you can in public cloud.

- These models largely take a page from what we see as a flawed SaaS pricing framework established by leading software companies like Oracle, Salesforce, Workday, SAP and others, where customers are locked in for a term with severe exit penalties or no way out;

- Cloud giants like AWS are taking a similar path for on-prem pricing (e.g. Outposts). The difference is that they have full like-to-like capability and are much more appealing to developers who can use the same APIs for their hybrid installations.

That said, we believe this is a necessary move for these vendors and we expect over time they’ll continue evolve their models. We frankly would like to see a starting point that is true pay-by-the-drink with an easy way for customers to try before they commit. We’d like to see vendors offer this and charge a premium with an incentive to make a longer term commitment (e.g. an on-prem version of reserved instances).

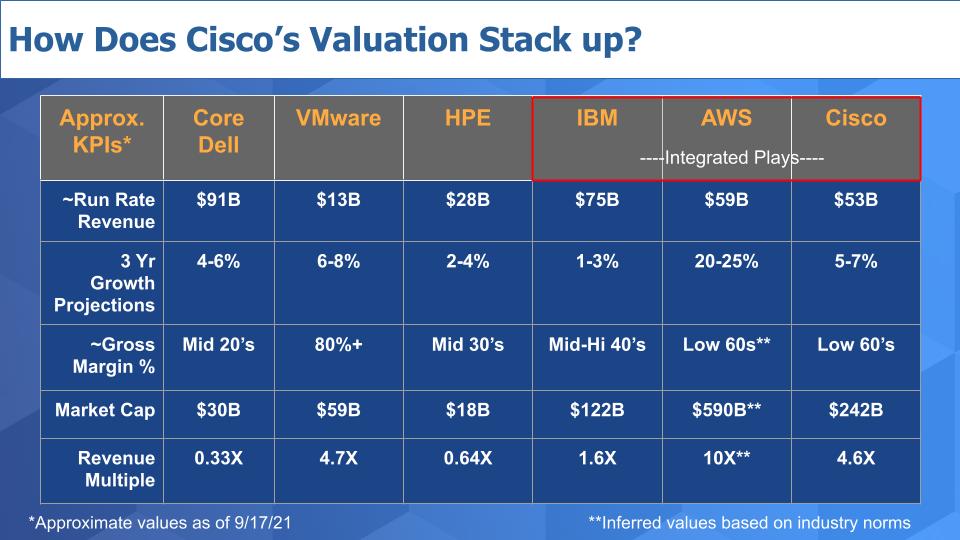

Compared to Most Peers, Cisco has an Awesome Financial Profile

The chart below compares five companies to Cisco. Core Dell – meaning without VMware, VMware, HPE…with IBM, AWS and Cisco as the three integrated plays.

The chart shows the latest quarterly revenue multiplied by 4X to get a revenue run rate. It shows a three year growth outlook, gross margin percentage, market cap and a revenue multiple.

The key points here are that: 1) Cisco has a pretty awesome business model – with 60%+ gross margins, strong operating margins (not shown here) in the mid 20’s, a higher growth rate than most of its peers and as such a much better revenue multiple than its peers.

For example core dell, which currently gets 33 cents on the revenue dollar, HPE, double that and IBM which is below 2X. Cisco’s revenue multiple rivals VMware’s, which is a pure software company. In a large part because VMware’s stock took a hit recently but still the point is obvious – Cisco has a great business.

For context we’ve added a hypothetical AWS, which blows away any company on this chart. We’ve inferred a market cap of nearly $600B, which frankly is conservative at a 10X revenue multiple given its margins and growth rate. AWS doesn’t report gross margins but its operating margins are comparable to Cisco’s so we’ve made what we think is a reasonable assumption for gross margin.

If AWS were a separate company it might have a market cap that approached $800B.

In this clip, Zeus Kerravala makes the following points about this data, summarized below:

- Comparing Cisco to HPE and Dell is understandable but the comparison is less valid today;

- Cisco has maintained its margins by innovating and done a good job of not getting commoditized;

- Cisco’s subscription model will only help underscore its innovation. If Cisco can continue to roll out the latest and greatest as part of its subscription offerings, customers will be more apt to adopt and that will put less pressure on margins.

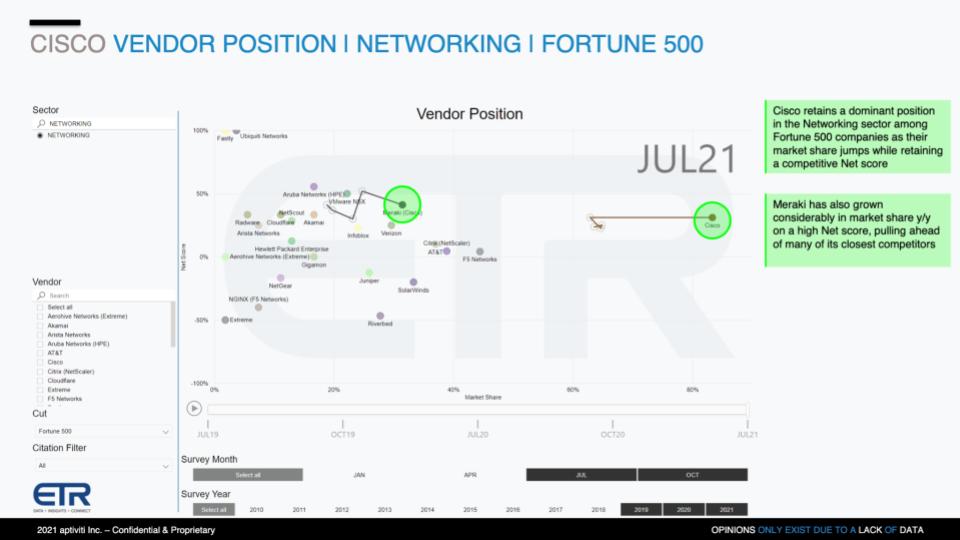

Cisco’s Margins Stem From a Dominant Position in Networking

One of the reasons Cisco has such a strong margin profile is it’s been able to grow both organically but it also it has a strong history of M&A. And it has a long track record of execution in networks that have earned it top spot in the market as shown in the ETR graphic below.

The chart shows Cisco’s dominant position in networking within the F500. It plots the companies in the ETR taxonomy on two dimensions – Net Score on the vertical axis, which is a measure of spending velocity, and Market Share on the X axis which measures presence in the survey. The point is Cisco is far and away the most pervasive player in the market. It has generally held a dominant position, although its core business has been under pressure over the last few years. But it maintains a respectable Net Score and consistently performs well for such a large company.

This clip highlights Zeus Kerravala’s comments on the competition, summarized below.

- Part of Cisco’s dominance simply stems from making good products;

- Historically the competition has been relatively benign with companies like 3Com and Nortel who aren’t independent firms anymore.

- Moving forward companies like VMware and AWS could be disruptive to Cisco;

- Arista is a much stronger company now and succeeding. Juniper bought Mist and is in better position. Even Extreme Networks who most people thought was dead a few years ago has made a number of acquisitions and is now a billion dollar company.

So while Cisco has done a great job of execution, they’ve also done a great job on the innovation side. Their competitive landscape, looking out over the next five years, is going to be more difficult than it has been over the previous five years. Largely, I think that’s good for Cisco. I think whenever Cisco’s pressed a little bit from competition, they tend to step on the innovation gas a little bit more. Even just the transition when VMware bought Nicira, that got Cisco’s SDN business into gear, like nothing else could have, right? So competition for that company, they always seem to respond well to it.

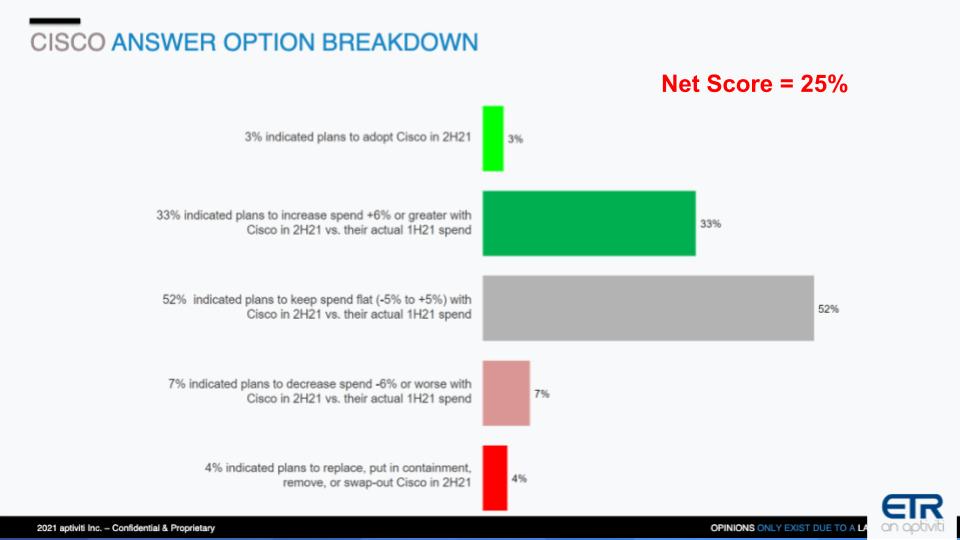

Breaking Down Cisco’s Net Score

Let’s briefly explain the derivation of Cisco’s Net Score in the survey. Cisco has been able to hold a respectable spending momentum profile despite its large size.

The chart above shows the granular components of Net Score. The lime green is new adoptions to Cisco, the forest green is spending more than 6%, the gray is flat spend, the pink is spending drops by more than 5% and red is leaving the platform. Cisco’s overall Net Score is 25%, which for a company of its size speaks to its relationships with customers. It has a fat middle in the gray area and, not surprisingly, a low percentage of new adoptions, but impressively, low defections.

Cisco is essentially “holding serve” in the survey, which is respectable for a company of its size.

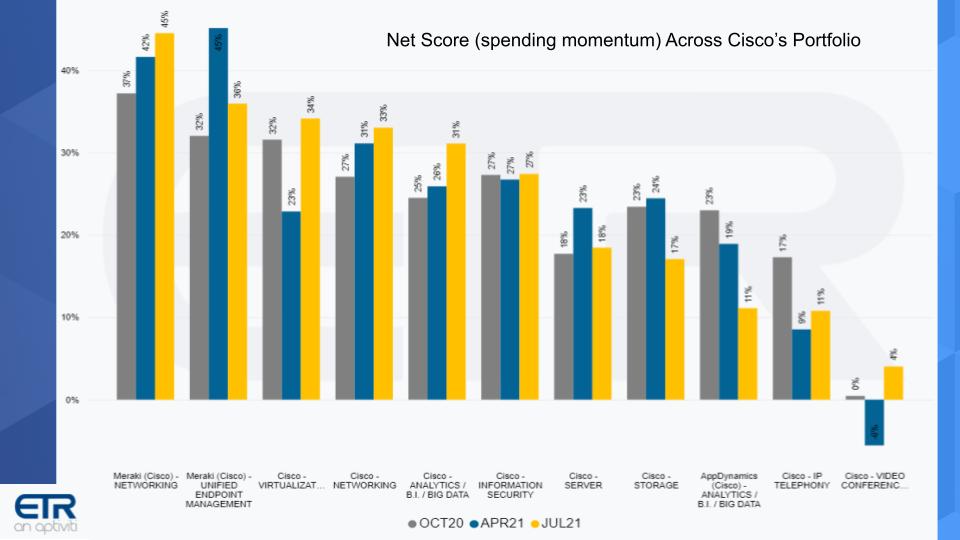

Spending Momentum in Cisco’s Portfolio – Meraki Shows Strong

Let’s look at spending momentum over time across Cisco’s portfolio.

The chart above shows Cisco’s Net Score within the ETR taxonomy over three survey periods. Meraki is very strong. Cisco’s virtualization business, its core networking, analytics, security…are all showing momentum. AppD is a bit concerning but that could be related to Cisco’s pivot to full stack observability and AppD being bundled there. However, practitioners have cited some concerns for AppD in that space as they’re seen as legacy. On the far right of the chart, Webex, while showing relative strength is not that high.

This clip shares the comments from Zeus Kerravala with further detail on Meraki below.

- Meraki arguably is one of the best acquisitions in Cisco’s history, perhaps rivaling Kalpana & Grand Junction, which resulted in the creation of Catalyst switches;

- Meraki’s revenue is comparable and might be larger than security, so that shows you the momentum it has.

- One of the lessons Meraki brought to Cisco is that simpler is better, sometimes;

- By putting Todd Nightingale in charge of all the networking business, it showed that Chuck Robbins understood that the things Meraki was doing were going in the right direction. They infuse a little bit of Meraki into the rest of the company and that’s certainly a good thing.

- The other point on the ETR data is when you think of the shift to hybrid work you would expect to see the traditional server and storage business under pressure because people aren’t building out data centers. Other areas related to hybrid work, hybrid cloud, especially security should remain strong.

- The WebEx data is interesting too, because it did show somewhat of a dip and then a rise. And think that’s indicative of what we’ve seen in the collaboration space since the pandemic came about. Cisco got caught a little bit flat-footed while zoom was taking off. But Cisco has caught up in features and now they really stepped on the gas.

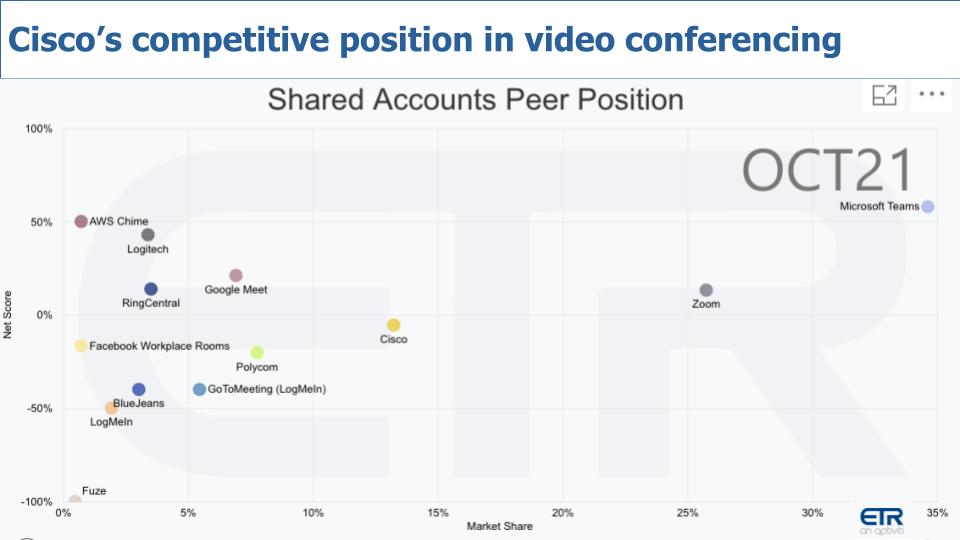

Speaking of Video Conferencing….

Below is a 2-dimensional view again showing Net Score against Market Share or pervasiveness of mentions for video conferencing in the ETR survey.

You can see Microsoft Teams is off the chart – literally. With Zoom well ahead of Cisco in terms of mentions presence. That could be a spate of freemiums by Zoom but it’s basically a 3-horse race in this game. Cisco is not trying to take Zoom head on, rather it’s making Webex a core part of a broader collaboration agenda.

This clip highlights Zeus Kerravala’s commentary on Webex, summarized below:

All of the vendors, including Teams, are going after the hybrid work experience. And if you believe the future is hybrid and not just work from home, then Cisco does have a pretty interesting advantage because it’s the only one that makes its own end points. Teams and Zoom do not. And so Cisco can deliver on that end to end experience…

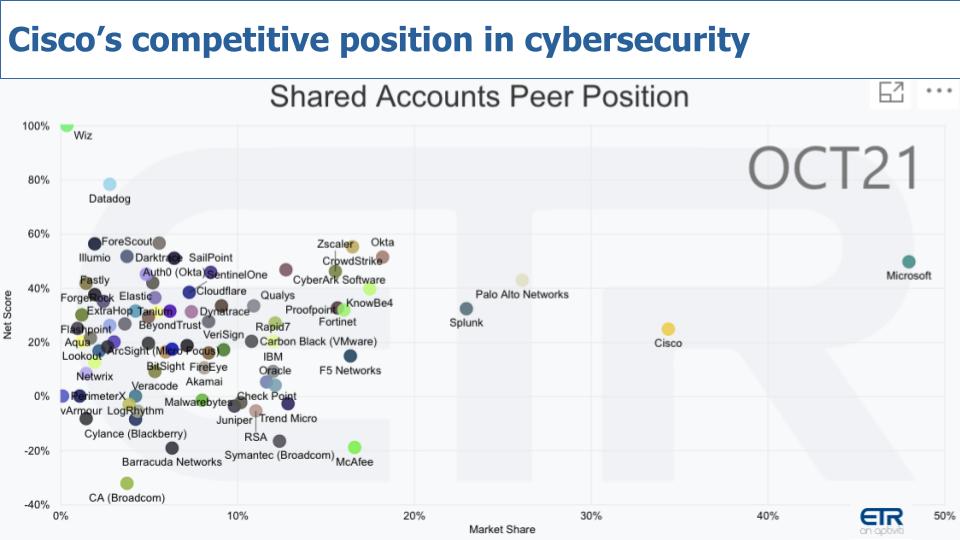

Security…Integrated Platform or Best of Breed?

We’d be remiss if we didn’t spend a moment on security. It’s a key part of Cisco’s business and we’ve seen several quarters of growth; although last quarter Cisco’s security growth was in the low single digits.

Cisco is a major player in security and this XY graph from ETR shows they have both a large presence and solid spending momentum. Not nearly as much momentum as Okta, Zscaler, Crowdstrike and some of the others we’ve featured in these episodes…but more than respectable. Security is critical to Cisco’s strategy and a big part of its subscriber base.

Cisco made the point at Analyst Day that this market is crowded and its goal is to simplify this picture and make it easier for customers to secure their data and apps. But that’s not trivial.

Zeus Kerravala comments on Cisco’s security posture in this clip and summarized in the quote below.

CISOs tell me you don’t have to have best of breed everywhere to have best in class threat protection. In fact, a lot of buyers will tell you that if you try and have best of breed everywhere, it actually creates a negative when it comes to threat protection; because keeping all the policies up to date is very difficult. The industry is moving more to a platform model and the challenge for Cisco is how do you get the customer to think of the network as part of the platform.

How can Cisco Win the Day in Cloud?

Let’s bring it back to cloud. We’ve talked about a number of the pieces of Cisco’s portfolio. We haven’t spent much time on full stack observability, which is a big push for Cisco with AppD, Intersight and the Thousand Eyes acquisition…and that plays into the cloud equation by assisting customers remediate application bottlenecks across estates.

Cisco has a number of cloud knobs it can turn…it sells core networking equipment to hyperscalers and it can be the abstraction layer to connect on-prem to the cloud, hybrid, across clouds and it’s in a good position with telcos too to go after the edge and 5G.

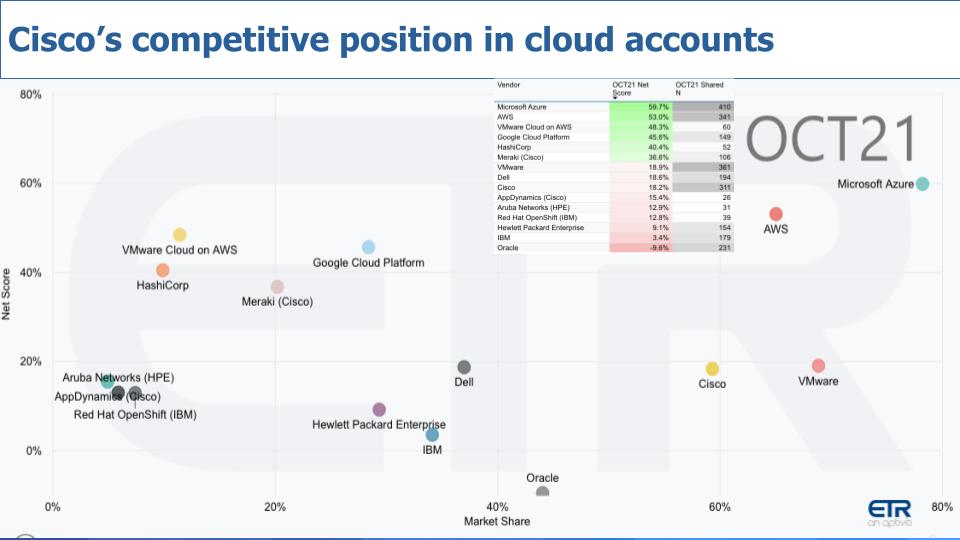

The chart below uses the same two dimensions – Net Score (spending velocity) and Market Share (pervasiveness) to compare competitors. This data displays vendor performance within hyperscale cloud accounts.

The chart above displays various companies that both compete and/or partner with Cisco at some level. The insert on the chart shows the raw data that positions each dot – the Net Score and Shared N – i.e. the number of accounts in the survey that responded.

The following points are noteworthy:

- Azure and AWS are dominant with GCP a distance third. Not only do those two have a large presence in the survey, they also have spending momentum on their platforms;

- VMware and Cisco are prominent because they have huge customer bases and, while they’re often on a collision course, there’s lots of room in cloud for multiple players;

- We’ve plotted some other Cisco properties like AppD and Meraki, which as we said is strong. And for context we’ve placed Dell, HPE, Aruba, IBM and Oracle in the chart;

- VMware Cloud on AWS is notable on the vertical axis and we added in HashiCorp because they’re a critical partner of Cisco’s and a multi-cloud enabler.

Here are two clips from Zeus Kerravala highlighting some of his thoughts on Cisco’s cloud strategy and prospects:

Clip 1 – The changing nature of cloud, the role of security and network evolution.

Clip 2 – Will more workloads going to public cloud mean less network spending with Cisco?

The bottom line for us is we believe Cisco is making moves to position it to thrive in cloud. The key positives and negatives we see Cisco for Cisco are the following:

Positives

- Playing offense in cloud. Cisco is looking at public cloud infrastructure as an opportunity on which it can build, rather than a threat. It can be the abstraction layer for hybrid, multi-cloud and edge;

- It is coming to the cloud from a position of strength in networking and has the opportunity to convince customers that it has the most trusted, secure, highest performance and cost-efficient platform;

- With its shift to a software and subscription model, Cisco has the potential to execute one of the more historically difficult transitions in IT– moving from a hardware to a software model. So far, Cisco’s progress is promising relative to the track record of others that have tried;

- The cloud is expanding and morphing into a ubiquitous, sensing, intelligent platform. Cisco’s large portfolio and innovation agenda fit nicely into this trend and significantly expand the company’s market opportunity;

- Cisco has a strong silicon design capability, which as we’ve reported, will become increasingly important for distributed cloud architectures in the future.

- Trusted brand. Networking is hard. Customers have faith in Cisco.

Negatives

- Cisco remains a highly complex company with a portfolio that continues to grow with aggressive M&A. Integration will remain a challenge for customers and will stretch Cisco’s R&D budget;

- This integration dynamic will in our opinion allow best of breed competitors to move faster than Cisco and challenge its innovation leadership;

- Cisco investors are hooked on and expect continued high margins which could constrict the company’s enthusiasm to go after seemingly low margin businesses that have massive growth potential – e.g. lower margin opportunities at the edge. Moreover, its focus on expanding its TAM and going after adjacent markets could open the door for competitors within its core business.

On balance we feel CEO Robbins is steering the company in the right direction with a strong focus on alignment with industry shifts. Cisco management is world class and while the company has much work ahead to navigate its transition, the prospects for Cisco, we believe, are extremely promising.

Keep in Touch

Many thanks to our colleague Zeus Kerravala for his collaboration. His expert analysis and deep knowledge of this space are greatly appreciated. Reach him at ZKresearch.com.

Remember we publish each week on this site and siliconangle.com. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Image credit: Mohsen

Note: ETR is a separate company from Wikibon/SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.